What Future US Monetary Policy Means For Gold Prices

Commodities / Gold and Silver 2011 Sep 19, 2011 - 02:59 AM GMTBy: Bob_Kirtley

Gold has traded in a choppy lateral motion recently, with prices sliding south over the past week or so. The market looks hesitant ahead of the FOMC meeting this week, with traders cautious not to take on too much prior to what could be a game changing announcement. Bears are cautious about getting too short in case Bernanke announces a significant easing of monetary policy and bulls share a similar sentiment in case the Fed announces less easing that the market currently expects. This lack of conviction coupled with some profit taking has contributed to the recent price action in gold.

Gold has traded in a choppy lateral motion recently, with prices sliding south over the past week or so. The market looks hesitant ahead of the FOMC meeting this week, with traders cautious not to take on too much prior to what could be a game changing announcement. Bears are cautious about getting too short in case Bernanke announces a significant easing of monetary policy and bulls share a similar sentiment in case the Fed announces less easing that the market currently expects. This lack of conviction coupled with some profit taking has contributed to the recent price action in gold.

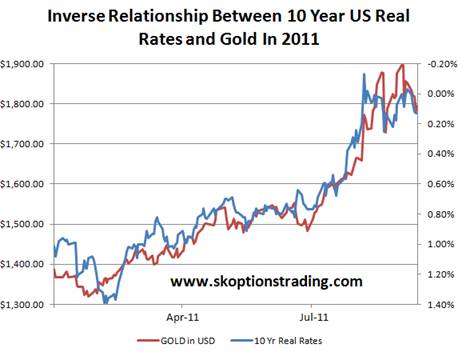

As our regular readers will know, we view US real interest rates as the primarily driver of gold prices over the medium term. Gold prices exhibit an inverse relationship with US real interest rates, with looser monetary policy leading to lower real interest rates and higher gold prices. Further discussion of this relationship can be found in our previous articles “The Key Relationship between US Real Rates and Gold Prices – 5th December 2010” and “Decline In US Real Rates To Send Gold Past $1800 – 18th July 2011”. We will not go into depth on the mechanics behind this relationship again in this article, but we note that the relationship is still intact and therefore it remains the cornerstone of our gold market analysis.

In order to form a view on where gold prices are going, we must also have a view on US real rates and US monetary policy. Our view for some time has been that the Federal Reserve would embark on further monetary easing as a response to a deteriorating economic outlook and persistently high unemployment. This view was based on the fact that the US yield curve had flattened to levels not seen since the Fed first hinted at QE2, as the chart below shows. A flattening yield curve is a sign of economic weakness, further discussion of the dynamics at play there can be viewed in our article entitled “US Yield Curve Flattening To Prompt Fed Easing and $1800 Gold -3rd August 2011”. The increased expectation of easing in the past two months has sent gold prices dramatically higher and real interest rates lower.

The question becomes not “Will the Fed ease?” but “To what degree will the Fed ease and what form will the easing take?” We will now take a moment to discuss the various options available.

The consensus expects that the Fed will implement “Operation Twist” – a policy that will see the Fed sell some of its holdings in shorter dated Treasury securities and buy longer dated Treasuries. This would be done with the intention of keeping longer term interest rates low and hopefully stimulating economic activity. Although this could be done without technically expanding the Fed’s balance sheet, it would dramatically increase the duration risk of the Fed’s portfolio and therefore still has similar effects to other forms of easing. However there are a number of other policies that could also be announced.

The Fed could simply expand the balance sheet again and simply buy more bonds, as they did in QE2, except target the long end of the yield curve. The goal of this policy would be to lower longer term interest rates. However such a goal could also be achieved by the Fed announcing a specific target or ceiling on a longer term interest rate. For example by announcing that they were targeting a yield of 1.5% of the 10 year notes. This would be achieved in a similar fashion to what happened at the August meeting when the Fed announced that they would not raise interest rates until 2013, effectively capping the 2 year note.

Another policy which could be announced is decreasing, or perhaps even eliminating, the interest paid to commercial banks on excess reserves. This rate (often referred to as the IOER) could be cut to 10bps to even to zero, in an attempt to spur lending. We are not sure how much of an effect this would have even implemented, and it would likely not have any significant effect on gold prices.

If Bernanke really wanted to enact a controversial policy, the Fed could buy foreign securities. By purchasing say peripheral European bonds and bailing out Europe, the Fed would reduce many concerns regarding Eurozone sovereign debt and weaken the US dollar. However we think that this policy is probably to unpalatable to the Fed and it is very unlikely that we will see a policy like this any time soon.

Although the technicalities of the easing are important, one must not overlook the psychology involved in the decision as well, which we view as at least equally important. Therefore we think there is a significant chance that the consensus view of the Fed stopping at Operation Twist may be in for a bit of a shock.

Thinking back to August 9th, the consensus was that the Fed would simply make a stronger commitment to keeping interest rates low for an “extended period” of time. But Bernanke went further than this and announced that he would keep rates near zero until mid 2013 – going further than the vast majority of people thought he would go.

Ben Bernanke has demonstrated on multiple occasions that he is not afraid of taking risks and he is willing to be very aggressive with monetary policy. With unemployment still above 9%, who can blame him? Regardless of whether one thinks that the Fed’s dual mandate of full employment and low inflation is right or not, the fact of the matter is that mandate is what it is and with unemployment at these elevated levels the Fed is not achieving its targets.

At the August meeting, we know both from the statement and meeting minutes that additional rounds of unconventional easing were discussed, plus Bernanke said at Jackson Hole that these such options were on the table. Therefore we feel that there is a significant risk that the Fed will ease much more than many expect. We do not think that the Fed will risk announcing something that is below market expectations, since markets would instantly tank. The Fed actively monitors what the market expects and if they were not going to announce anything then the Fed would have tactically hinted this prior to this week, to prevent markets being shocked to the downside.

The fact that it is going to be two day meeting also increases the probability that we are going to see something significant. The last time a two day meeting was called was in December 2008 and QE1 was put into action. We think Bernanke will use the extra time to convince the dissenters (there were three at the August meeting) that further aggressive easing is necessary.

So what happens after the Fed eases and what does it mean for gold?

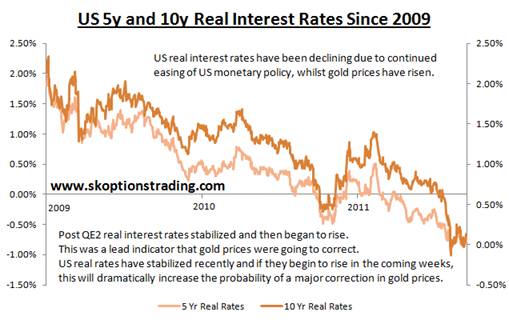

Of course monetary easing is bullish for gold prices, but once the easing is announced, digested and effectively priced in, gold prices will be dependent on future expectations of monetary easing and therefore the future economic outlook. If Fed easing, whatever form it takes, is successful at improving the economic outlook then this is not bullish for gold prices over the medium term. An improving economic outlook would probably see longer term US real interest rates increase, the yield curve steepen (unless longer term rates are specifically capped) and therefore flow through to a decrease in gold prices.

This happened after QE2, when the flow of economic data was much more positive and US real rates began to rise. This initially capped gold prices, before causing a decline of about 11% in early 2011, a similar scenario could unfold after this Fed meeting. Also increasing US real rates in late 2009 and early 2010 was accompanied by gold prices declining some 14% in early 2010.

So considering all of the above, what is our trading strategy going forward?

As a reminder, all of our trading recommendations are based on options traded on US markets. Therefore when considering gold we trade options on GLD. We do not trade gold mining companies (and have rarely touched the mining stocks since May 2008) or options on gold mining companies for reasons discussed in our previous article, “Are Gold Stocks The Real Barbarous Relic? – 11 Jul 2011”.

We are maintaining a moderate long position on GLD through the FOMC meeting. Our exposure is however significantly lower than it was in the run from $1600 to $1800 when we felt that the risk-reward was far more skewed to the upside than it is at present. Nonetheless we maintain a sizeable long bias and still expect gold prices to reach $2000 in 2011, but most likely within the next month. Our reluctance to take a more aggressive position is not reflective of a lack of conviction that gold will reach $2000, but more due to our view that risk looks more symmetric than it did a couple of months ago.

Our plan for after the FOMC meeting will be largely dictated by the language in the statement and the behaviour of US real interest rates in the weeks following. An exceptionally accommodative statement coupled with significantly declining US real rates would likely see us increasing our gold exposure. However an announcement of easing that is within a reasonable range of current market expectations will not cause us to increase our gold exposure. In fact a scenario where the statement is more accommodative that expected, but US real rates are rising would cause us to reduce our gold exposure. Rising US real rates and rising gold prices would see us selling into gold’s strength, as we view US real rates as the lead indicator here.

If a situation of increasing US real rates and rising gold prices persists and we have exited our long positions then we would be considering a short bias. We are not comfortable with outright aggressive short positions on gold due to the significant event risk, but we would be open to selling call spreads into such a market. These limited risk trades carry positive Theta and would look particularly attractive if near term calls are heavily bid and we see a backwardation of the volatility curve. Further discussion of the recent examples of backwardation in the gold volatility curve can be found in our previous article, “The Market Dynamics That Sent Gold Past $1800 – 15th August 2011”. A market with a vol curve in backwardation and skewed heavily towards calls is prime for selling call premium in our opinion, since both are symptomatic of a frothy market packed with speculative longs. Such a market could occur in the next month or so.

To stay updated on our market commentary, which gold stocks we are buying and why, please subscribe to The Gold Prices Newsletter, completely FREE of charge. Simply click here and enter your email address. (Winners of the GoldDrivers Stock Picking Competition 2007)

For those readers who are also interested in the silver bull market that is currently unfolding, you may want to subscribe to our Free Silver Prices Newsletter.

DISCLAIMER : Gold Prices makes no guarantee or warranty on the accuracy or completeness of the data provided on this site. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This website represents our views and nothing more than that. Always consult your registered advisor to assist you with your investments. We accept no liability for any loss arising from the use of the data contained on this website. We may or may not hold a position in these securities at any given time and reserve the right to buy and sell as we think fit. Bob Kirtley Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.