Dividends Provide An Stock Investors Return Bonus

InvestorEducation / Dividends Aug 22, 2012 - 07:44 AM GMT

With all things being equal, dividend paying common stocks provide their shareholders a return bonus, or what some might like to call a kicker, over an equivalent common stock that pays no dividend. Many investors do not see it this way, as they tend to think of the dividend providing them their return. However, the stock market capitalizes earnings whether a company pays a dividend or not. Moreover, we contend that the market will value a given company’s earnings based on their past and future prospects for growth, again, regardless of whether a dividend is paid or not.

With all things being equal, dividend paying common stocks provide their shareholders a return bonus, or what some might like to call a kicker, over an equivalent common stock that pays no dividend. Many investors do not see it this way, as they tend to think of the dividend providing them their return. However, the stock market capitalizes earnings whether a company pays a dividend or not. Moreover, we contend that the market will value a given company’s earnings based on their past and future prospects for growth, again, regardless of whether a dividend is paid or not.

To clarify our point further, an investment in a common stock typically offers their shareholders two components of return. The first component is the capital appreciation component or the increase (or decrease) in the stock’s value over time. The second component is the dividend, or lack thereof, that the company pays to shareholders in cash, typically once a quarter. The two added together equal the shareholders’ total return. On the one side, we have the capital growth component and on the other side the income component.

Now, here is the primary point behind this article. If you examine two companies with equivalent rates of earnings growth, where one pays a dividend and the other does not, the dividend payer will provide their shareholders a higher total return. In other words, we’re suggesting that both stocks will provide equivalent capital appreciation when measured over a time period when the market is behaving rationally. We would define this as a time period when both stocks were being priced at fair value in the beginning and in the end. Consequently, the stock that pays a dividend to its shareholders is providing them a return bonus or kicker.

What we are about to say next may come as heresy to the devout dividend growth investor. Nevertheless, the facts speak for themselves and we ask that they try to look at the total picture with an open mind, and eyes. In either case, dividend paying or not, the bulk, or majority, of total return will be provided by the capital appreciation component. This is why we are saying that dividends are a kicker or bonus return. In other words, capital appreciation is the cake and dividends (if any) are the icing.

As a point of further clarification, this principle applies to the true dividend growth stock. We would define a true dividend growth stock as a company that has historically grown earnings at an above-average growth rate, and is expected to continue growing earnings at an above-average rate in the future. To clarify even further, low growth dividend paying stocks like utilities will often provide their shareholders the bulk of their returns through dividends. This is due to the low growth nature of their earnings which typically leads to subpar capital appreciation.

(If you would like to test this last statement regarding utilities, follow this link to Addendum To - Investing in Eastern Utility Stocks - Do Today’s Valuations Make Sense, Part 4)

A Picture Is Worth 1000 Words

To illustrate the validity of the thesis behind this article, we are going to once again rely on the F.A.S.T. Graphs™ earnings, price (and dividends) correlated research tool. This powerful “tool to think with” was designed to graphically, and therefore, instantaneously portray the important principles underlying the total return that shareholders can expect from a given common stock. More importantly, they were designed so that each of the two components of return, capital appreciation and dividend income, could be visually exposed independently and therefore, returns easily and quickly calculated.

The Total Return Component

The total return component is driven by the market pricing a company according to its earnings achievements. Therefore, the orange earnings justified valuation line on each of the following graphs represents what we call the True Worth™ or what others might call the intrinsic value of each sample company, again, based on the market capitalizing its total earnings. Simply stated, when the black monthly closing price line touches the orange earnings line, fair value is present.

Focusing on this earnings and price relationship will provide an instantaneous perspective of capital appreciation as long as fair value is present in the beginning and the end. All that the reader has to do is look immediately to the right of each graph to find the company’s earnings growth rate listed and use it to easily estimate returns.

Consequently, without any mathematical computation, the reader should understand that the capital appreciation component will precisely equal, or at least closely correlate, to the company’s earnings growth. Therefore, when price starts on the orange line and is on the orange line at the end, whatever the earnings growth rate is, the capital appreciation will also be (within minor valuation adjustments).

In order to demonstrate this as clearly as possible, we had to carefully pick historical time frames where earnings and price were correlated (the price touching the orange line) both at the beginning and at the end. Although we could not do this with absolute precision, as you will soon see we were able to accomplish it within reasonable margins of error.

In other words, the price and earnings relationships we are showing are not perfect matches, but very close. However, in order to carry out this objective with the examples chosen, we had to draw some of our charts where we ended them through calendar year-end 2011 because valuation was in alignment at that time (thereby eliminating any 2012 data points). This was done in order to visually articulate the principle that we are hypothesizing.

The Dividend Income Component

Interestingly enough, the dividend income component is also driven by and is a function of the company’s earnings achievements. Even though dividends are paid out of earnings, we intend to demonstrate that the market eventually capitalizes the full measure of the company’s earnings even though a portion has been paid out. Therefore, the dividend component becomes, as our thesis indicates, an extra or bonus piece of return.

In order to depict this as vividly as possible, we chose to illustrate the full measure of each company’s earnings (the green shaded area with the orange line on top) and then illustrate the dividend component separately. Therefore, we calculate the dividends paid out of earnings (light blue shaded area) and show them as additional return by stacking them on top of the green shaded earnings area on the graph (Note: The orange line represents the fair value of the company’s earnings, while the green shaded area represents the total earnings). We believe this serves as a constant reminder that even though dividends come out of earnings, the capital appreciation component of the dividend paying stock is not reduced or diminished by the dividend.

A quick word about ex-dividend dates are in order. Although it is true that a company’s stock price will fall at precisely the level of its declared dividend, this is only relevant for that brief moment in time. In any other time during the quarter, and usually almost immediately following the ex-dividend date, the company’s stock price will be once again capitalized based on its total earnings. In other words, over the majority of the time that a dividend paying stock trades, their shareholders’ profits are not penalized by dividends. Therefore, and in truth, the dividend provides additional return above and beyond the company’s earnings growth.

Examples Of The Dividend Bonus

Before we move on to presenting specific graphical evidence of our thesis that dividends are a bonus, a few qualifying remarks are in order. As previously alluded to, this article focuses on dividend growth stocks, which we define as dividend paying companies with above-average earnings growth. Therefore, we will be primarily presenting companies with above-average, to significantly above-average, historical total returns and earnings growth rates. It is from this class of dividend paying stock where the majority of return comes from growth of principle.

On the other hand, even for low growth dividend paying stocks such as utilities, the capital appreciation component is often low because of the low growth rate of the company’s earnings. (If you would like to test this last statement regarding low growth utilities, follow this link to Addendum To: Investing in Central Utility Stocks, Do Today’s Valuations Make Sense, Part 3.)

Furthermore, the dividend component is usually above-average with utility stocks, so cumulative total dividend returns may be equal to or even exceed capital appreciation. Nevertheless, the principle that dividends represent a bonus return remains valid.

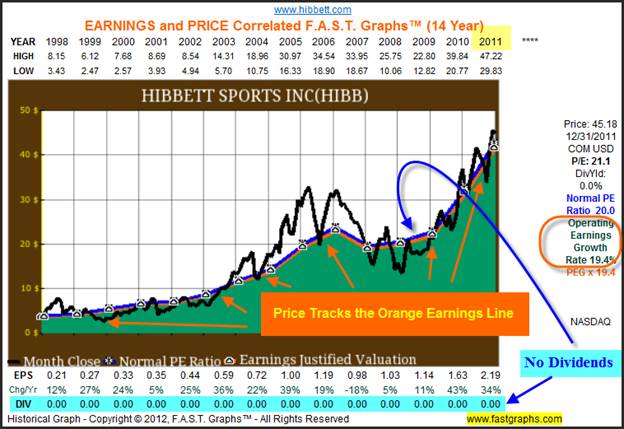

Our first set of examples compares two very fast growing businesses with one paying a dividend and the other not. Our nonpaying example is Hibbett Sports Inc (HIBB), a sporting goods store operating predominately in the Southeast, Southwest, Mid-Atlantic and Midwest regions of the United States. As we can clearly see by the earnings and price correlated graphic below, the company’s earnings growth rate (the orange line) has averaged over 19% for the years 1998 to 2011. But most importantly, we see that the market has priced the company in accordance with its earnings growth. Note the lack of a dividend as highlighted at the bottom of the graph (also no light blue shaded area on graph).

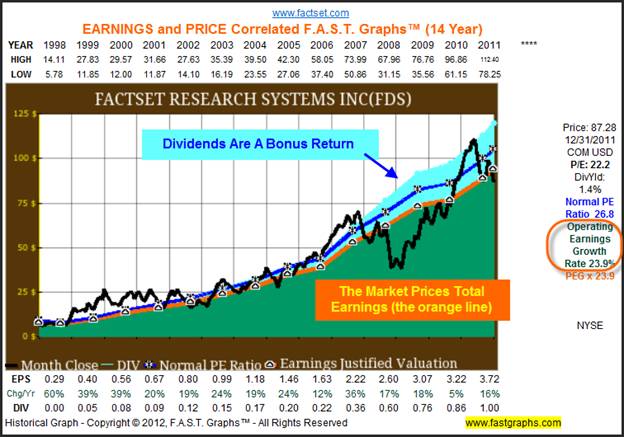

Our dividend paying example, FactSet Research Systems Inc (FDS), combines integrated financial information, analytical applications, and client service to enhance the workflow and productivity of the global investment community. Their services are offered to Investment Managers, Hedge Funds, Investment Bankers, Wealth Managers, Pension Plans, Private Equity Groups, Government Agencies, Academics and numerous other members of the financial community.

Just as we saw in our first example, the market has capitalized the full measure of FactSet Research Systems Inc’s earnings just as it did for Hibbett Sports Inc. However, our attention is immediately drawn to the light blue shaded area or dividends. Since the company’s price was close to the earnings line at the beginning and at the end, we can assume that capital appreciation should approximate the 20% plus earnings growth rate. But the key point behind this article is to note that dividends provide returns that are in addition to price appreciation as depicted by the light blue shaded area.

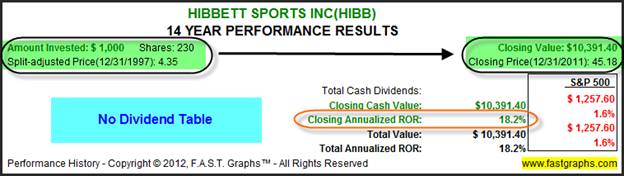

Next let’s examine the total return performance of each of our two samples. Our first example, Hibbett Sports Inc, grew earnings at 19% and therefore, generated capital appreciation at 18.2% that was a close approximation to its earnings growth rate of 19.3%. Note that there are no dividends or dividend cash flow table listed. This is another design feature of the F.A.S.T. Graphs™ research tool.

A $1000 investment made on December 31, 1997 would have purchased 230 shares of Hibbett Sports Inc. at $4.35 per share. By December 31, 2011 the price of the stock had appreciated approximately ten-fold to $45.18 per share. This turned a $1000 investment into $10,391.40 for a compounded annual rate of return of 18.2% per year, which again, was although just under but closely approximating the 19% earnings growth rate. Even without a dividend, Hibbett Sports Inc. generated shareholder returns that were significantly higher than the average company as measured by the S&P 500.

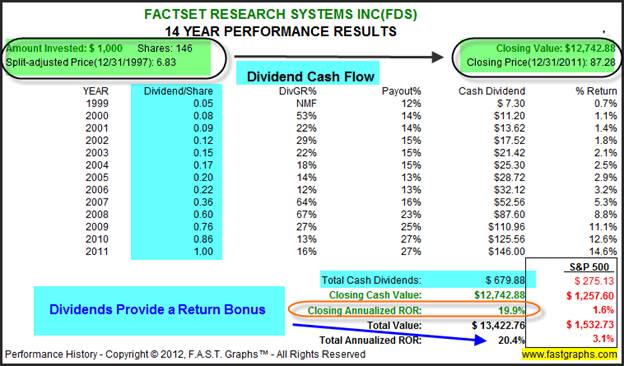

Now, as we turn to our dividend paying example, FactSet Research Systems Inc., we discover a more complex performance record. We still discover that a $1000 investment on December 31, 1997 would have purchased 146 shares at a price of $6.83 per share. Then, just as we saw with our first example, the share price on December 31, 2011 grew to $87.28 per share. Thereby generating a capital appreciation component, that is more than twelve-fold larger than our original investment.

Interestingly, our dividend paying, and therefore theoretically more conservative stock, actually grew faster notwithstanding the fact that it was paying dividends. This explains the greater capital appreciation component with FactSet Research Systems Inc. However, we further discover the dividend cash flow table which clearly illustrates the impact, and the additional rate of return, that shareholders received through dividends.

With our next two examples we will look at a slightly shorter time frame covering the eight-year period calendar years 2004 through 2011. Once again, our sample companies in the time frames covered were specifically chosen because they clearly illustrate the reality behind our thesis that dividends represent a bonus return to shareholders. To repeat, if you have two companies with approximately the same rate of earnings growth that are purchased at fair value, and one pays a dividend, its shareholders will receive a bonus return over shareholders of the non-dividend paying or otherwise equivalent company.

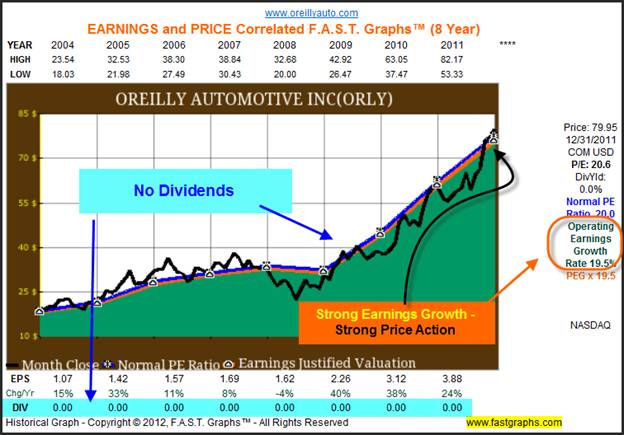

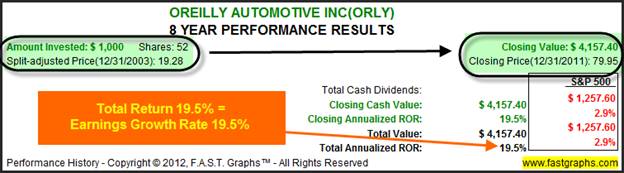

O’Reilly Automotive Inc (ORLY) is a fast growth automotive aftermarket parts and tools retailer that grew earnings at a rate of 19.5% per annum between 2004 in 2011. Clearly, we see that the company’s stock price has tracked its earnings growth, and anytime when the price moved above or below the earnings line it quickly returned. However, the important point is that the market capitalized the full measure of the company’s earnings in the long run.

Consequently, shareholders of O’Reilly Automotive Inc enjoyed a return over this eight-year period of time that was virtually identical to the company’s earnings growth rate. But since there were no dividends being paid, only the capital appreciation component applies.

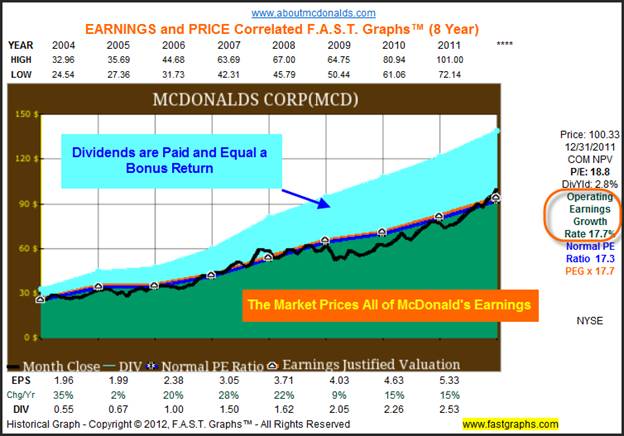

Our next example, McDonald’s Corp (MCD), also enjoyed very fast earnings growth of 17.7% from 2004 to 2011. However, we see by the light blue shaded area on its graph that they also paid their shareholders a nice dividend. With this graph we can clearly see a visual example of how dividends represent an extra, or bonus, rate of return. The stock price very closely tracks and correlates to earnings with the price close to touching the orange line at the beginning and only slightly above the orange line at the end.

Therefore, once again we see undeniable evidence that the full measure of McDonald’s earnings are being priced by the marketplace. If dividends do not represent additional return, then it would logically follow that the normal PE ratio (the dark blue line) would be below the orange earnings line illustrating that the market did not price the portion of earnings that were paid in dividends. Instead, we see that both the orange earnings justified valuation line and the blue normal PE ratio line are almost perfectly coinciding.

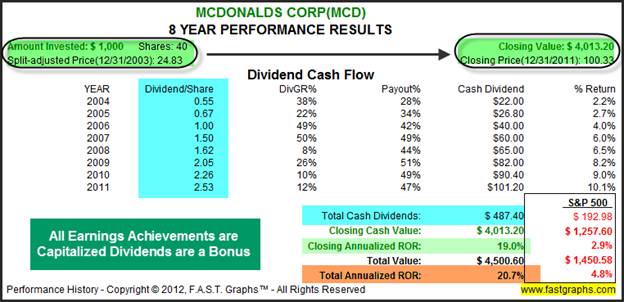

Now as we examine McDonald’s performance, we find capital appreciation slightly exceeding earnings growth due to the very modest overvaluation at the end of the period. However, and most importantly, we see that dividends in this example contribute additional return.

Just like we saw with O’Reilly Automotive above, McDonald’s shareholders received the full value of their earnings growth from the marketplace. Furthermore, their dividend payments representing a portion of earnings paid out to shareholders, did not penalize the capital appreciation component of the stock. Instead, dividends made a meaningful and additional contribution to McDonald’s Corp’s exceptional total shareholder returns during this time period.

Summary

Take away all the day-to-day noise associated with investing in stocks and the stock market and you will discover that in the long run fundamentals matter. In other words, inevitably shareholders of stock in a publicly traded company will be rewarded in direct proportion to how well the business performs on an operating basis. The better the business does, the better the shareholders will be rewarded.

The primary measurement of business performance is profitability, otherwise known as earnings. It is earnings that the market ultimately prices a stock by, and it is from earnings that dividends are paid. However, it is our contention that the market does not price the stock according to their dividend policy, they price the stock according to their earnings power. Therefore, if and when a company does pay a dividend, it represents a nice bonus to total shareholder returns.

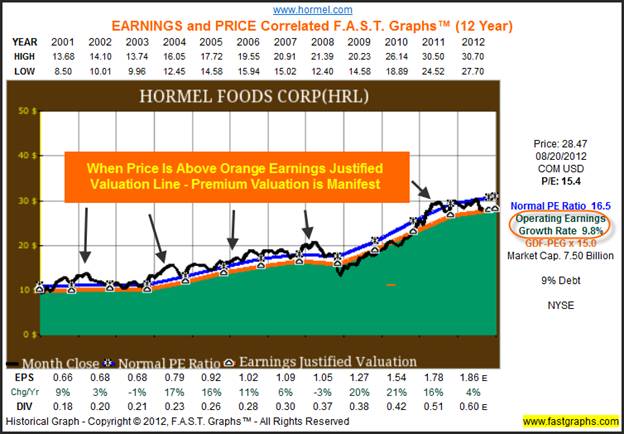

When we review the earnings and price correlated graph on Hormel Foods Corp (HRL) below we see that the black monthly closing stock price line tracks the orange earnings justified valuation line. Furthermore, we also see that, in fact, the market has tended to more-often-than-not applied a premium valuation to this moderate growing blue-chip. With this iteration, dividends have been excluded from the analysis.

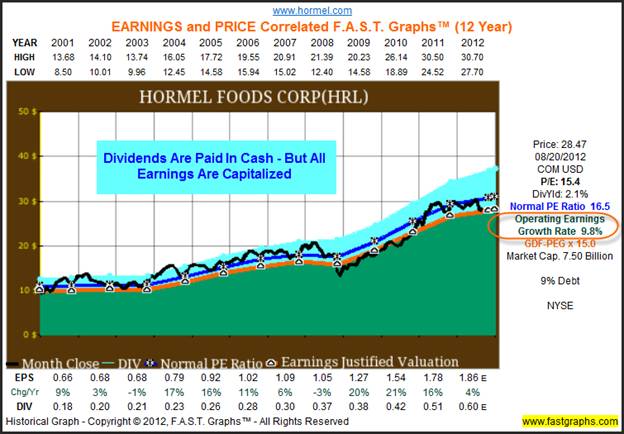

With our next graphic we simply redraw the graph with dividends (the light blue shaded area) added. Remember, our first graph and this graph show the market applying a premium valuation. However, the difference here is that we see how dividends, when they are stacked on top of earnings, represent the additional return dividends provide the shareholders. As you look at this graph and the other dividend paying stocks included in this article, you should keep in the back of your mind that the light blue shaded area actually represents a cash payment to shareholders.

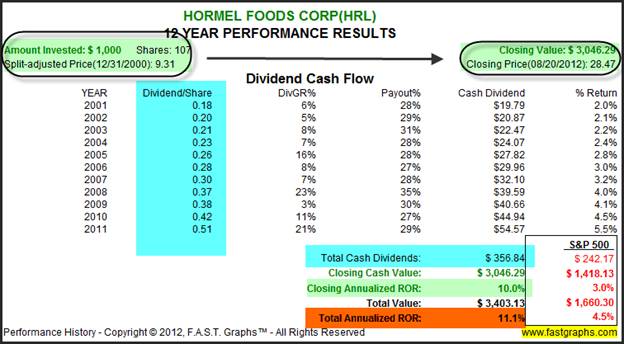

Now as you examine the performance associated with the earnings and price correlated graph above, note that capital appreciation (closing annualized ROR) is almost identical to the company’s earnings growth rate. Therefore, all of the company’s earnings are being priced by the market, even those earnings that were paid out in dividends. However, we can also clearly see how the dividends represent the bonus this article has presented within its thesis.

Conclusions

We have long held that investing in common stocks is all about investing in the underlying businesses. When looked at this way, it is only logical to place more of your focus and attention on the results of the companies you are invested in instead of worrying about day-to-day variations in its market price. Because, whether it is capital appreciation you are after, dividend income or both, they are all generated by the profits from the businesses.

Regarding dividend paying stocks, it’s great to get, as Will Rogers so eloquently once put it, a return of your capital as well as a return on your capital. The major object of this article was to point out that dividend paying stocks are capable of providing both a return of original capital invested and a return on your money. On the other hand, dividend paying stocks are fully capable of being great total return generators. From this perspective, we see the dividend as a nice quarterly bonus. But whether dividend paying or not, the principles of valuation must always be given careful consideration.

Disclosure: Long MCD at the time of writing.

By Chuck Carnevale

Charles (Chuck) C. Carnevale is the creator of F.A.S.T. Graphs™. Chuck is also co-founder of an investment management firm. He has been working in the securities industry since 1970: he has been a partner with a private NYSE member firm, the President of a NASD firm, Vice President and Regional Marketing Director for a major AMEX listed company, and an Associate Vice President and Investment Consulting Services Coordinator for a major NYSE member firm.

Prior to forming his own investment firm, he was a partner in a 30-year-old established registered investment advisory in Tampa, Florida. Chuck holds a Bachelor of Science in Economics and Finance from the University of Tampa. Chuck is a sought-after public speaker who is very passionate about spreading the critical message of prudence in money management. Chuck is a Veteran of the Vietnam War and was awarded both the Bronze Star and the Vietnam Honor Medal.

© 2012 Copyright Charles (Chuck) C. Carnevale - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.