Ben Bernanke Financial Crisis Hero?

Stock-Markets / US Federal Reserve Bank Dec 01, 2013 - 04:45 PM GMTBy: John_Mauldin

The true measure of a career is to be able to be content, even proud, that you succeeded through your own endeavors without leaving a trail of casualties in your wake. – Alan Greenspan

The true measure of a career is to be able to be content, even proud, that you succeeded through your own endeavors without leaving a trail of casualties in your wake. – Alan Greenspan

If economists could manage to get themselves thought of as humble, competent people on a level with dentists, that would be splendid. – John Maynard Keynes

And He spoke a parable to them: "Can the blind lead the blind? Will they not both fall into the ditch?" – Luke 6:39-40

Six years ago I hosted my first Thanksgiving in a Dallas high-rise, and my then-90-year-old mother came to celebrate, along with about 25 other family members and friends. We were ensconced in the 21st floor penthouse, carousing merrily, when the fire alarms went off and fire trucks began to descend on the building. There was indeed a fire, and we had to carry my poor mother down 21 flights of stairs through smoke and chaos as the firemen rushed to put out the fire. So much for the advanced fire-sprinkler system, which failed to work correctly.

I wrote one of my better letters that week, called "The Financial Fire Trucks Are Gathering." You can read all about it here, if you like. I led off by forming an analogy to my Thanksgiving Day experience:

I rather think the stock market is acting like we did at dinner. When the alarms go off, we note that we have heard them several times over the past few months, and there has never been a real fire. Sure, we had a credit crisis in August, but the Fed came to the rescue. Yes, the subprime market is nonexistent. And the housing market is in free-fall. But the economy is weathering the various crises quite well. Wasn't GDP at an almost inexplicably high 4.9% last quarter, when we were in the middle of the credit crisis? And Abu Dhabi injects $7.5 billion in capital into Citigroup, setting the market's mind at ease. All is well. So party on like it's 1999.

However, I think when we look out the window from the lofty market heights, we see a few fire trucks starting to gather, and those sirens are telling us that more are on the way. There is smoke coming from the building. Attention must be paid.

I was wrong when I took the (decidedly contrarian) position that we were in for a mild recession. It turned out to be much worse than even I thought it would be, though I had the direction right. Sadly, it usually turns out that I have been overly optimistic.

This year we again brought my now-96-year-old mother to my new, not-quite-finished high-rise apartment to share Thanksgiving with 60 people; only this time we had to contract with a private ambulance, as she is, sadly, bedridden, although mentally still with us. And I couldn't help pondering, do we now have an economy and a market that must be totally taken care of by an ever-watchful central bank, which can no longer move on its own?

I am becoming increasingly exercised that the new direction of the US Federal Reserve, which is shaping up as "extended forward rate guidance" of a zero-interest-rate policy (ZIRP) through 2017, is going to have significant unintended consequences. My London partner, Niels Jensen, reminded me in his November client letter that,

In his masterpiece The General Theory of Employment, Interest and Money, John Maynard Keynes referred to what he called the "euthanasia of the rentier". Keynes argued that interest rates should be lowered to the point where it secures full employment (through an increase in investments). At the same time he recognized that such a policy would probably destroy the livelihoods of those who lived off of their investment income, hence the expression. Published in 1936, little did he know that his book referred to the implications of a policy which, three quarters of a century later, would be on everybody's lips. Welcome to QE.

It is this neo-Keynesian fetish that low interest rates can somehow spur consumer spending and increase employment and should thus be promoted even at the expense of savers and retirees that is at the heart of today's central banking policies. The counterproductive fact that savers and retirees have less to spend and therefore less propensity to consume seems to be lost in the equation. It is financial repression of the most serious variety, done in the name of the greater good; and it is hurting those who played by the rules, working and saving all their lives, only to see the goal posts moved as the game nears its end.

Central banks around the world have engineered multiple bubbles over the last few decades, only to protest innocence and ask for further regulatory authority and more freedom to perform untested operations on our economic body without benefit of anesthesia. Their justifications are theoretical in nature, derived from limited-variable models that are supposed to somehow predict the behavior of a massively variable economy. The fact that their models have been stunningly wrong for decades seems to not diminish the vigor with which central bankers attempt to micromanage the economy.

The destruction of future returns of pension funds is evident and will require massive restructuring by both beneficiaries and taxpayers. People who have made retirement plans based on past return assumptions will not be happy. Does anyone truly understand the implications of making the world's reserve currency a carry-trade currency for an extended period of time? I can see how this is good for bankers and the financial industry, and any intelligent investor will try to take advantage of it; but dear gods, the distortions in the economic landscape are mind-boggling. We can only hope there will be a net benefit, but we have no true way of knowing, and the track records of those in the driver's seats are decidedly discouraging.

For this week's Thanksgiving weekend letter I offer a section from my new book (co-authored with Jonathan Tepper), called Code Red. You can see a video interview with Jonathan Tepper and me and buy the book here, or of course you can go to Amazon and read the reviews. And the book is in all the bookstores. Needless to say, it will make an excellent gift for clients, family, and friends.

At the end of the letter I will provide a link to a free webinar I am doing next week with Jonathan Tepper and Lacy Hunt, hosted by Altegris Investments, on the implications of ZIRP and other unconventional policies; but now let's jump into Code Red. In this section, we deal with the topic of central banking and its failures and ponder the implications of continuing to give the same people ever more authority and responsibility. This is from Chapter 5, called:

Arsonists Running the Fire Brigade

In the old days, central banks raised or lowered interest rates if they wanted to tighten or loosen monetary policy. In a Code Red world everything is more difficult. Policies like ZIRP, QE, LSAPs, and currency wars are immensely more complicated. Knowing how much money to print and when to undo Code Red policies will require wisdom and foresight. Putting such policies into practice is easy, almost like squeezing toothpaste. But unwinding them will be like putting the toothpaste back in the tube.

We'll admit that we're having too much fun criticizing central bankers, the Colonel Jessups of the Code Red world. But please don't just take our word for it when we tell you that they're clueless. Let's look at what others have written.

In 2009 Congress created the Financial Crisis Inquiry Commission to uncover the causes and consequences of the financial catastrophe that almost brought down the world financial system. They roundly condemned the Federal Reserve:

We conclude this crisis was avoidable. The crisis was the result of human action and inaction…. The prime example is the Federal Reserve's pivotal failure to stem the flow of toxic mortgages, which it could have done by setting prudent mortgage lending standards. The Federal Reserve was the one entity empowered to do so and it did not…. We conclude widespread failures in financial regulation and supervision proved devastating to the stability of the nation's financial markets.

Not surprisingly, public confidence in the Fed has plummeted.

The Federal Reserve performed disastrously before the Great Financial Crisis, but almost all central banks were asleep at the wheel. The record of central banks around the world leading up to the Great Financial Crisis was an unmitigated disaster. All countries that had housing bubbles and large bank failures failed to spot them beforehand. In the case of England, where almost all major banks went bust (some rather spectacularly!) and required either nationalization or fire sales to foreign banks, the Bank of England never saw the crisis coming. Let's look at what The Economist has to say about central bank failures:

In 1996 the Bank of England pioneered financial-stability reports (FSRs); over the next decade around 50 central banks and the IMF followed suit. But according to research cited by Howard Davies and David Green in "Banking on the Future: The Fall and Rise of Central Banking," published last year, in 2006 virtually all the reports, including Britain's, assessed financial systems as healthy. In the basic function of identifying emerging threats, "many central banks have been performing poorly," they wrote.

According to published reports, the Bank of England only learned about the bankruptcy of one huge bank after another a few days before the actual public announcement. So much for staying on top of the situation. The regulators were captured by the very institutions they were supposed to regulate, with neither the banks of the regulators understanding the serious nature of the problems they were creating with their actions.

Housing bubbles swelled and burst everywhere: Spain, Ireland, Latvia, Cyprus, and the United Kingdom. Countries that had to recapitalize or nationalize their banks were broadsided by a disaster they did not anticipate, prepare for, or take action to prevent. In the case of Spain, even after the crisis unfolded, the Bank of Spain acted like a pimp for its own banks. It insisted nothing was wrong and proceeded to help its banks sell loads of crap to unsuspecting Spaniards in order to recapitalize the banks. (We apologize for our language, but there is no other word besides crap that properly characterizes selling worthless securities to poor pensioners – well, there are, but they are even less suitable for public consumption).

In fairness, central bankers did save the world after the Lehman Brothers bankruptcy. The money printing that the Federal Reserve oversaw after the failure of Lehman Brothers was entirely appropriate to avoid another Great Depression. But giving them credit for that is like praising an arsonist for putting out the fire he started.

Figure 5.3 Ben Bernanke: The hero who saved the world

The failure of central banks makes it all the more remarkable that they were given even more responsibility in the wake of crisis. Since 2007 central banks have expanded their remits, either at their own initiative or at governments' behest. They have exceeded the limits of conventional monetary policy by buying massive amounts of long-dated government bonds, mortgage-backed securities, and other assets. They have also taken on more responsibility for the supervision of banks and the stability of financial systems.

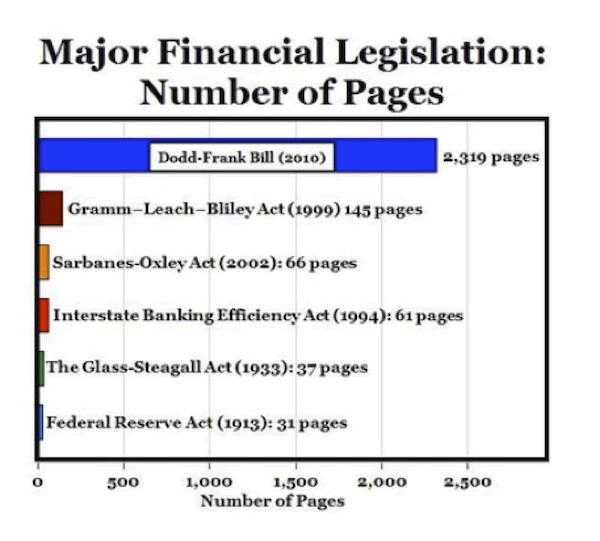

The Banking Act of 1933, more popularly known as the Glass-Steagall Act, forced a separation of commercial and investment banks by preventing commercial banks from underwriting securities. Investment banks were prohibited from taking deposits. Until it was repealed in 1999, the Glass-Steagall Act worked brilliantly, helping to prevent a major financial crisis. It was replaced by the Graham-Leach-Bliley Act, which ended regulations that prevented the merger of banks, stock brokerage companies, and insurance companies. The American public's interests were thrown to the wolves of Wall Street, and the Fed and the Clinton administration gave the middle finger to financial stability.

After the Great Financial Crisis, Congress could have simply reinstated Glass-Steagall. The act was only 37 pages long, but it had worked incredibly well. Instead, after an orgy of bank lobbying and Congressional kowtowing to the bankers who had brought the world to the brink of a global depression, Congress passed the Dodd-Frank Act. It is over 2,300 pages long; no one is sure what is in it or what it means; and it has added a dizzyingly complex tangle of regulations and bureaucracy to what should have been a simple, straightforward reform of the financial sector. (The act is so long and complicated that it was nicknamed the "Lawyers' and Consultants' Full Employment Act of 2010.") You will hardly be reassured to learn that the Federal Reserve's powers were expanded through Dodd-Frank.

Please note that it was the same banks and investment firms that lobbied to repeal Glass-Steagall in 1999 that so aggressively and successfully lobbied for the Dodd-Frank Act. While there are some features contained in the plan that are good, the basic problems still remain. Industry insiders were able to assure that business as usual could continue. And to judge from their profits, it has done so remarkably well.

Figure 5.4 Major financial legislation: number of pages

The Fed didn't need more powers. In the years leading up to the Great Financial Crisis, the Fed already had almost all the tools it needed to prevent the subprime debacle. It simply failed to use them. You could call that lapse nonfeasance, dereliction of duty, going AWOL, or anything other than doing their duty. If you don't believe you are capable of recognizing a bubble in advance, then all the additional regulations in the world won't make any difference in preventing a bubble. Dodd-Frank merely gave them more regulations not to enforce. It is the mindset that needs changing, not simply the regulations.

According to the Financial Crisis Inquiry Commission, the Federal Reserve failed to use the tools at its disposal to regulate mortgages or bank holding companies or to prevent the abusive lending practices that contributed to the crisis. The central bank didn't "recognize the cataclysmic danger posed by the housing bubble to the financial system and refused to take timely action to constrain its growth," the report said. It also "failed to meet its statutory obligation to establish and maintain prudent mortgage lending standards and to protect against predatory lending."

The most sordid part of the Great Financial Crisis was not the extreme failure by central banks to regulate. The most egregious violation of the public interest came in the form of the massive subsidies and aid the central banks gave to the banking system when the crisis was underway. The great journalist and essayist Walter Bagehot argued in the mid-19th century that during a financial crisis central banks should lend freely but at interest rates high enough to deter borrowers not genuinely in need, and only against good collateral. During the crisis, the Fed and other central banks lent trillions of dollars at zero cost against the shoddiest of collateral. And the Fed went out of its way to provide gifts to Wall Street banks via the back door. For example, when AIG went bust, Timothy Geithner decided that the US taxpayer should pay out credit default swaps to AIG's counterparties at full price. Goldman Sachs was given a parting gift to $10 billion. Ge ithner did not even negotiate a haircut. The money went to dozens of banks, many which were not even American. It is no wonder Geithner became well-known as "Wall Street's lapdog."

Our good friend Dylan Grice wrote a fascinating piece on what happens when you have too many rules and too little common sense. In a Dutch town called Drachten, local government decided to take out all traffic lights and signs. They hoped people would pay more attention to the road rather than fixate on rules and regulations. They were right. In Drachten there used to be a road death every three years, but there have been none since traffic light removal started in 1999. There have been a few small collisions, but these are almost to be encouraged. A traffic planner explained, "We want small accidents in order to prevent serious ones in which people get hurt." Let's see what Dylan has to say about the lessons for capital markets:

You might be thinking that traffic lights don't have anything to do with the markets we all work in. But I think they do. Instead of traffic lights and road signs think rating agencies; think Basel risk weights for Core 1 and Core 2 bank capital; think Solvency 2; or think of the ultimate market regulators of our currencies – the central banks – and the Greenspan/Bernanke "put" which was once imagined to exist. Haven't these regulators provided the same illusion of safety to financial market participants as traffic safety tools do for drivers? And hasn't this illusion of safety been even more lethal?

Wouldn't it be nice if central bankers thought more like Drachten town planners? But central bankers and parliaments prefer extensive rules to a common-sense approach.

Unlike the planners of Drachten, the Federal Reserve and central banks around the world issue extensive sets of regulation, fail to enforce them, encourage everyone to speed, and then when crashes happen they protect as many banks as possible from the consequences of their own actions.

The Federal Reserve is in desperate need of reform. This doesn't mean that politicians should be deciding interest rates or that banking supervision should be taken away from central banks. But central bankers should be answerable to the public for how they do their jobs. Accountability has been completely missing throughout the entire crisis. Almost all central banks failed to do even the basics of their job. The regulations they created, especially in Europe, made it possible for banks to take massive risk and make huge profits that ultimately had to be bailed out by taxpayers.

They believe the banks and other institutions they were regulating when they showed the models which they created which demonstrated conclusively there was no risk. Everyone, bankers and regulators, believed we were in a new era, for the old rules of common sense didn't apply. Central bankers didn't need more rules or regulations. They failed miserably at even carrying out the simple job they had. The regulatory functions of central banks should be treated like those of any other regulatory agency. It is critical that we hold central bankers accountable for their management of the banking system.

One of the most disastrous battles of World War I was the British Gallipoli campaign in Turkey in 1915. It was utterly devastating, leaving more than 50,000 British wounded and almost 100,000 dead. Winston Churchill, first lord of the Admiralty, was one of the architects of the campaign. In the wake of the outcome, he resigned his post to become a soldier in the war. Churchill was a humble man who felt he was at fault. He was honorable. But if Churchill had been a central banker, he would never have had to accept responsibility or resign. He would have kept his job and been given even more far-reaching powers and a big pay raise to boot.

For the past few years, central bankers have been living large. The same people who brought us the Great Financial Crisis are now bringing us a world of Code Red policies and financial repression. The arsonists are running the fire brigade.

Where is the central banker who has apologized for contributing to the crisis or for being asleep at the wheel? Given how disastrous their performance has been, it is extraordinary that the same cast of characters is still running the show. Central bankers are lucky that they still have jobs. As far as we are aware, no central banker was fired for incompetence or mismanagement. Many have retired and are now enjoying generous pensions and highly paid consulting careers advising investment funds as to what their former colleagues might do next.

Central bankers have had plenty of time to discuss the financial crisis since 2008, but they have provided only scholarly disquisitions as to what went wrong in the banking crisis, without accepting any responsibility at all. At no time have any central bankers admitted that they might have ignored the warning signs of excessive debt, kept interest rates too low for too long, ignored bubbles in housing markets, failed to regulate banks correctly, or proved themselves even mildly incompetent.

Not only were central bankers not fired, many were promoted instead and given pay raises. Timothy Geithner, who headed the Federal Reserve Bank of New York, not only failed to regulate a host of banks that needed massive government bailouts but was an active apologist for Wall Street banks. For his efforts he was promoted to Secretary of the Treasury under President Obama. In Europe, Spanish central bankers stand out as perhaps the most incompetent ever, having overseen dozens of banks that created the biggest housing bubble in European history and having failed to recognize problems not only before but after they happened. Bankers like Jose Viñals, Jose Caruana, and others were given plum jobs at the IMF and the ECB after being asleep at the wheel in Spain.

Granting extra powers to central banks without a change in the philosophy behind their management is like encouraging an irresponsible teenager. Imagine your teenage son borrowed the family car and crashed it, and instead of punishing him you bought him a new Ferrari to test drive. Conventional monetary policies are like a sturdy old family station wagon, but Code Red policies are like a modified Ferrari 288 GTO capable of hitting 275 miles per hour. Given how spectacularly central banks failed during the Great Financial Crisis, it blows the mind that they've been handed the keys to a faster set of wheels.

One last thought. You might get from reading this that we are against rules and regulations. Far from it. We just like very simple, workable rules. Reinstate Glass-Steagall. Limit the ability of banks to create leverage, and require even more capital as they get larger. Banks that are systemically too big to fail are too big, period. Take away the incentive to grow beyond what is prudent for the deposit insurance scheme of a nation to maintain. Allowing bankers to take the profits and then hand taxpayers the losses in a crisis is not good policy, even if it is bolstered by 1,000 pages of regulations written by lawyers and bank lobbyists who then proceed to "massage" them in order to do what they want to anyway.

But, alas, such hopes may remain dreams deferred until there is yet another crisis and taxpayers are asked to absorb even greater losses (but we can always hope!). So, in the meantime, as prudent investors and managers, we must be aware of the realities we face. The saying in Africa is that it is not the lion you can see that is the danger, instead it is the one hidden in the grass that leaps out at you as you try to escape the one you see. Later we will talk about a few strategies that can help you handle the risks that crouch hidden in the grass.

Navigating the Unknown: What Investors Need to Know for 2014

I'd like to remind all US accredited investors or FINRA-licensed advisors to register and join me for an exclusive upcoming Mauldin Circle webinar on Tuesday, December 3, at 1:00 p.m. EST/10:00 a.m. PST. This highly anticipated event, "Navigating the Unknown: What Investors Need to Know for 2014," aims to provide investors with key perspectives for making portfolio decisions in 2014. I've invited my Code Red co-author, Jonathan Tepper; renowned economist Lacy Hunt; and alternatives expert Jon Sundt, CEO & President of Altegris, to join me. This panel represents a terrific mix of economic and investment viewpoints with a focus on investor solutions. My goal is for listeners to walk away with greater clarity about the Code Red world and an actionable perspective on global markets and the potential for diversifying into alternatives in 2014. Understanding and managing uncertainty shouldn't be a ny more complicated than necessary!

If you are already a Mauldin Circle member, a webinar invitation has already been sent directly to you by email. If you are unable to listen in to the live discussion, be sure to register so that you can receive the replay information. A replay will be available to all qualified registrants. If you are not a member of the Mauldin Circle and are an accredited investor or a FINRA-licensed advisor, please join today. The Mauldin Circle program provides exclusive access to alternative investment managers and other thought leaders. In addition, members receive exclusive access to special events and conferences. Upon qualification by my partners at Altegris, you will receive an email invitation. I apologize for limiting this discussion to accredited investors and investment advisors, but we must follow the rules and regulations. I look forward to having you at this exclusive Mauldin Circle event. (In this r egard, I am president and a registered representative of Millennium Wave Securities, LLC, member FINRA.)

New York, Geneva, Saudi Arabia, Dubai, and Northwest Canada

I will be in New York this week for meetings and a keynote speech at the CIO Investment Summit, where I will also be on a panel with Jim Grant, whom I will actually get to meet for the first time. I've been a Jim Grant fan for decades, and it will be a delight to sit next to him and hear him speak live. My friend Mark Yusko has put together a powerhouse one-day conference that also includes Kyle Bass and John Paulson.

The following week features a quick trip to Seattle for my partners at Altegris Investments. Then I'll zip back to Dallas to change suitcases and head to Geneva for a few days before returning home for Christmas. Then in early January I leave for the Middle East to speak at MASIC's CSR Policy Forum and to meet investors and leaders in the area. I also plan to visit Dubai for a few days – I've been told it is a place I must see to believe. If you are in either town, drop me a note.

It is time to hit the send button. I am almost moved into my new abode, although the office will be finished next week while I am in NYC, so I am writing this missive from my old one-bedroom office apartment. Waking up this morning in the new place to look out over downtown Dallas on a beautiful morning was a true pleasure. I feel home for the first time in a long time and am surprised at how good it feels. Maybe it's just the newness, but I hope not. This very first day saw some 50-odd family and friends gather to christen the place, spilling food and drink; and there was the madness of a dozen young kids cavorting and another dozen people working happily on the massive spread. Hard to believe that the day before some 15 construction artisans ("workers" seems so pedestrian a title for the level of work they do) were busy hammering, sawing, painting, and applying stone and wood and wire to get the place almost ready to move into – which we proceeded to do. And then we cooked and prepared for the big day.

Have a great week. I am looking forward to December in NYC, always a magical experience.

Your looking forward to leftover turkey sandwiches analyst,

John Mauldinsubscribers@MauldinEconomics.com

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2013 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.