Why a Strong U.S. Dollar is the Ultimate Economic Stimulus

Economics / US Dollar Nov 09, 2014 - 10:53 AM GMTBy: Clif_Droke

Earlier this year commodities prices were fairly buoyant thanks in part to strong demand in Asia. The strength didn’t last long, however, and by summer weakness was evident in Europe and China. Global growth slowed considerably in the months leading up to October, when oil plunged below $90/barrel for the first time since 2012. Apart from weakening global demand and the growth of energy supplies (thanks to fracking), the strengthening U.S. dollar has accelerated this trend.

Earlier this year commodities prices were fairly buoyant thanks in part to strong demand in Asia. The strength didn’t last long, however, and by summer weakness was evident in Europe and China. Global growth slowed considerably in the months leading up to October, when oil plunged below $90/barrel for the first time since 2012. Apart from weakening global demand and the growth of energy supplies (thanks to fracking), the strengthening U.S. dollar has accelerated this trend.

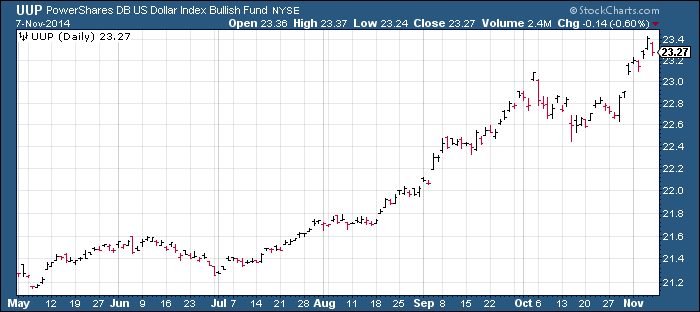

The strong dollar has resulted in an interesting feedback loop: as the value of the dollar increases a combination of steady U.S. economic growth and corresponding weakness in Europe and China make the dollar attractive to foreign investors. Since many developing countries are dependent on commodities, dollar strength tends to benefit the U.S. economy at the expense of other countries. Below is a chart of our favorite dollar proxy, the PowerShares U.S. Dollar ETF (UUP), which shows the extent of the dollar’s impressive rise this year.

One of the key variables of the financial markets from roughly 2001 until 2011 was a persistently weak dollar. The weak dollar of those years, moreover, tended to be bullish for equity prices. The reason for this is because the 2001-11 decade encompassed most of the commodity price boom (or bubble, as some would have it). Many of the stocks which outperformed in 2001-11 were of commodity-related companies such as mining and oil/gas producers and explorers. The oil stocks were one of the single biggest contributors to the run-up in the S&P 500 of the years prior to the credit crisis, so it made sense that a weak dollar benefited these companies since it boosted export prices and increased the bottom line.

In recent years, the commodities bubble has deflated and the stock market’s gains have come largely from technology, financial sector, and non-commodity related stocks. A stronger dollar typically benefits these types of companies, as was the case in the booming corporate economy of the late 1990s. It appears that the strong dollar/strong stock market dynamic of those years is making a comeback and it couldn’t be happening at a more opportune time. The middle class in desperate need of a “bailout” and a strong dollar is arguably the best form of stimulus for consumers. It will also help companies which cater to consumers by increasing profit margins and generating higher sales volumes.

A dollar bull market, in other words, benefits everyone except for those in the natural resource sector. While a strengthening dollar may seem at face value to be deflationary, the danger of a rising dollar index is only acute when the long-term economic cycle (the 60-year cycle) is in its “hard down” phase. As of last month a new long-term up-cycle was born and deflation from here will become less and less of a threat, at least in the U.S. Indeed, “deflation” in terms of falling commodity prices and consumer prices is actually beneficial to consumers when the 60-year cycle is in its ascending phase. So we needn’t worry about the long-term impacts of a rising dollar index from here either as investors or as consumers.

Dollar weakness has also had the dual benefit of lowering fuel prices, which in turn is benefiting consumers. Citigroup analyst Ed Morse estimates that if oil prices stabilize near current levels, the typical U.S. household will receive the equivalent of a $600 annual tax cut. Another recent Citigroup analysis concluded that oil that’s 20 percent cheaper than the 3-year average price amounts to a $1.1 trillion annual stimulus to the global economy.

Goldman Sachs estimates that every 10 percent drop in the oil price stimulates 0.15 percent more consumption in the world economy; moreover, it also increases demand for oil consumption by half a million barrels per day. Clearly then commodity market weakness is more of a blessing than a curse for the consumer-based U.S. economy.

Another factor which is helping the consumer economy heading into 2015 is the drop in mortgage rates. Below is a graph courtesy of the St. Louis Fed which shows the 30-year conventional mortgage rate going back to the year 2006. The recent drop in mortgage rates to below 4 percent has spurred a refinance rush. Demand for refinancing rose 23 percent in the seven days through Oct. 17, according to the Mortgage Bankers Association. The share of home loan applicants seeking to refinance jumped to 65 percent – the highest since November 13 and up from 59 percent the previous week, according to the MBA.

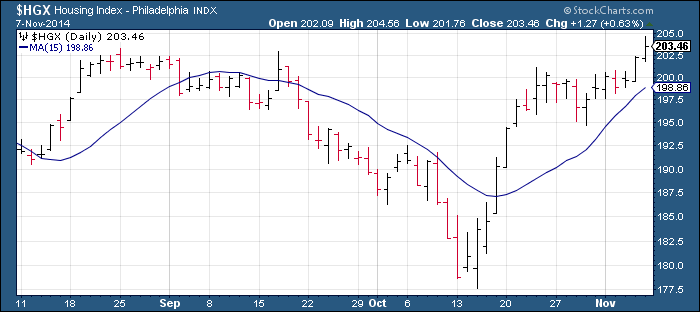

According to Businessweek, application volumes in the week ended Oct. 10 doubled from a week earlier at mortgage lender Quicken Loans. Mark Vitner, senior economist at Wells Fargo Securities, believes the refinancing “boomlet” will provide an added lift for the financial sector in the fourth quarter. The strength of the refinancing demand can also be seen in two invaluable charts, which happen to have important implications for the overall financial sector. The first chart example is of the PHLX Housing Index (HGX), which shows a potentially bullish consolidation pattern.

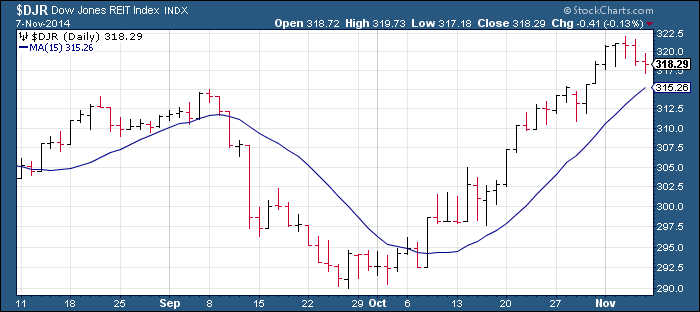

The next chart exhibit shows the progression of the Dow Jones Equity REIT Index (DJR) over the last past few weeks. The REITs tend to be more immediately sensitive to changes in interest rates and often lead the broader housing sector. Note that DJR is in a relative strength position versus both the HGX as well as the S&P 500.

Both DJR and HGX suggest that the housing market, which showed some weakness in the third quarter, will likely benefit from the recent mortgage rate drop as well as last month’s long-term Kress cycle bottom. Next year could finally be the year that sees prospective middle class homebuyers emboldened enough to finally begin taking the plunge back into the mortgage market once again.

Some Wall Street analysts question how much longer the bull market in equities can continue if the dollar remains strong. They would do well to recall the magnificent period between 1997 and 1999, which was the last notable period of dollar strength. At that time the U.S. economy was white hot, stock prices were on a relentless upward march, energy prices were low and the U.S. was the undisputed leader in attracting foreign capital inflows. Again I would emphasize the point that as long as the long-term Kress cycles aren’t declining, a strong dollar can only boost America’s economic and financial market prospects.

Unfortunately, due to the reticular nature of the global economy there is no such thing as “everyone’s a winner.” Gains in the U.S. economy can only come at the expense of foreign countries whose economies are much more highly sensitive to commodity prices than ours. As the dollar strengthens and energy prices plunge, for instance, oil-dependent nations such as Russia and Venezuela will weaken. On the other hand, industrialized nations which are highly dependent on exports stand to gain as the dollar strengthens. History teaches that a persistently strong dollar will eventually undermine several important foreign economies, which will in turn lead to the next global crisis. (As one historian has remarked, “The world economy progresses only at the expense of crisis.”)

From the standpoint of middle class America, the strong dollar couldn’t be more welcome. The middle class deserves a break after all the suffering of the last six years, even if it means other countries are suffering at our expense. Americans, after all, have no reason to feel any allegiance to the global economy and are rightly concerned with their own prospects. With any luck, the strong dollar will continue into 2015 just as the U.S. enters the “sweet spot” of the decadal rhythm.

There has never been a losing year for stocks in the Five year of the decade; moreover, there has hardly been a losing year after a Congressional election year. And with the 60-year cycle having recently bottomed, all the major yearly Kress cycles will be up next year. Combine this with a domestic economy that is showing signs of wanting to finally break out and 2015 is shaping up to be an across-the-board “good” year for most Americans, the first in quite some time.

Mastering Moving Averages

The moving average is one of the most versatile of all trading tools and should be a part of every investor's arsenal. The moving average is one of the most versatile of all trading tools and should be a part of every investor's arsenal. Far more than a simple trend line, it's a dynamic momentum indicator as well as a means of identifying support and resistance across variable time frames. It can also be used in place of an overbought/oversold oscillator when used in relationship to the price of the stock or ETF you're trading in.

In my latest book, "Mastering Moving Averages," I remove the mystique behind stock and ETF trading and reveal a completely simple and reliable system that allows retail traders to profit from both up and down moves in the market. The trading techniques discussed in the book have been carefully calibrated to match today's fast-moving and sometimes volatile market environment. If you're interested in moving average trading techniques, you'll want to read this book.

Order today and receive an autographed copy along with a copy of the book, "The Best Strategies For Momentum Traders." Your order also includes a FREE 1-month trial subscription to the Momentum Strategies Report newsletter: http://www.clifdroke.com/books/masteringma.html

By Clif Droke

www.clifdroke.com

Clif Droke is the editor of the daily Gold & Silver Stock Report. Published daily since 2002, the report provides forecasts and analysis of the leading gold, silver, uranium and energy stocks from a short-term technical standpoint. He is also the author of numerous books, including 'How to Read Chart Patterns for Greater Profits.' For more information visit www.clifdroke.com

Clif Droke Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.