The Next Recession Will Blow Out the Budget

Economics / Recession 2018 Oct 14, 2016 - 05:39 PM GMTBy: John_Mauldin

The odds that the next US President will face a recession during his or her first four years in office are quite high. Maybe not in the first year, but it’s highly unlikely he or she will get more than two to three years without one.

The odds that the next US President will face a recession during his or her first four years in office are quite high. Maybe not in the first year, but it’s highly unlikely he or she will get more than two to three years without one.

Given this fiscal reality and the dwindling number of arrows left in the Federal Reserve’s monetary policy quiver, the administration will have a hard time dealing with the fallout from a recession.

My friend Mike Shedlock recently pointed out an interesting discrepancy between the gross domestic product (GDP) and the gross domestic income (GDI). Mish says, “The basic difference between the two is that GDP measures what the economy produces—goods, services, technology, intellectual property—while GDI measures what the economy makes, tracking things like wages, profits, and taxes.”

In theory, the two numbers should be the same, as both are designed to measure the aggregate growth of the economy. GDP measures what the economy produces, GDI measures what it takes in.

Since GDI and GDP use different data sources, these readings are subject to measurement error. And there are good reasons for economists and market participants to focus on GDI rather than GDP.

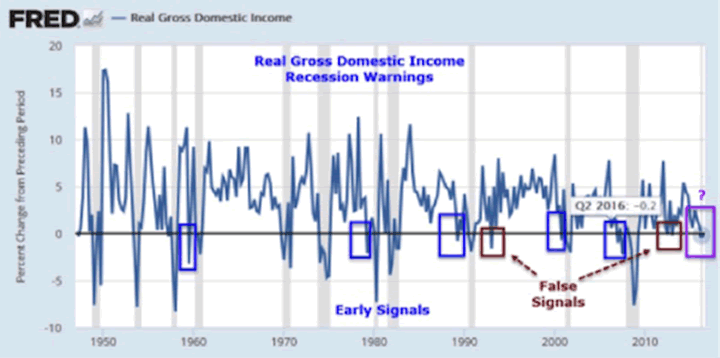

GDI signals a recession is coming

A main difference in GDI and GDP inputs is tax receipts. GDI takes into account taxes on production and imports, as well as subsidies, net interest, and miscellaneous payments.

But, Mish points out an interesting discrepancy between GDP and GDI. The third estimate for second-quarter GDP was bumped up to 1.4%. But, GDI was marked down to -0.2%. That is a rather large discrepancy.

Since the 2008 financial crisis, first-quarter GDP has consistently lagged growth during the second, third, and fourth quarters. And the whole point of the government “seasonally adjusting” the data is to smooth out these variances and give markets and the public a more reliable, consistent picture of the country’s economic health.

Given the repeated failures of the first quarter to be anything other than a disappointment, it seemed that something was off. As currently tabulated, GDP was a big disappointment in the first quarter. As currently tabulated, GDI showed an economy that is still growing.

But, Mish notes that GDI may now be signaling that a recession is impending. Please note that he points out that while a negatively growing GDI is not an infallible indicator, it is right more often than wrong. So we should at least have our antennae up.

Mish then gives us a chart for GDI:

Whereas real GDP was revised up 0.3 percentage points, real GDI was revised lower by 0.4 percentage points, to -0.2%.

A quick glance at the recession bars in the above chart shows what negative GDI numbers traditionally mean.

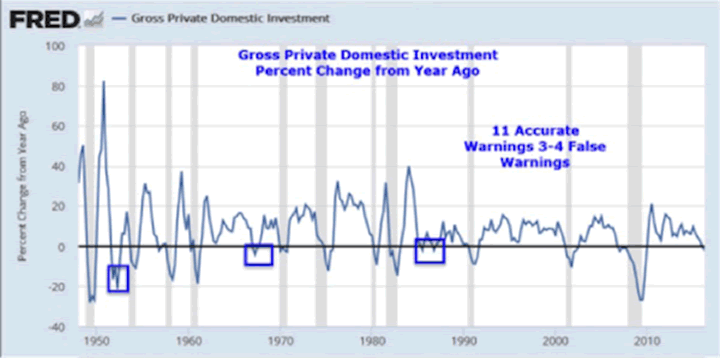

And then he goes on to note that this signal is being confirmed by the data for real private gross domestic investment.

Real private investment (not to be confused with income) is a measure of investment in the real economy, not under the influence of massive amounts of government spending. The numbers are not pretty.

There are many other indicators that show the economy is getting softer (even as you can find indicators that lead you to have a more sanguine, if not overly optimistic, view).

But the point is that the economy is running at stall speed. Any shock that comes from outside the US—from Europe or Japan or China—or from an initiation of interest rate hikes by the Fed (which would force a repricing of bonds and equities), could set off a recession that would become self-reinforcing.

The deficit is approaching $1 trillion

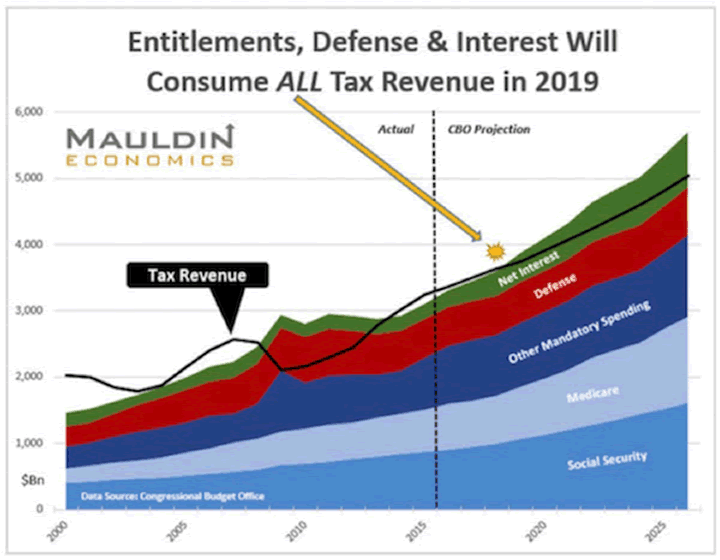

Let’s look at fiscal reality. Sometime in the first year of the next presidential term, the US national debt will top $20 trillion. The deficit is running close to $500 billion, and the Congressional Budget Office projects that figure to rise. Add another $3 trillion or so in state and local debt. As you can see, the interest on that debt is beginning to add up, even at the extremely low rates we have today.

Sometime in 2019, entitlement spending, defense, and interest will consume all the tax revenue collected by the US government. That means all spending for everything else will have to be borrowed. The CBO projects the deficit will rise to over $1 trillion by 2023. By that point, entitlement spending and net interest will be consuming almost all tax revenue, and we will be borrowing to pay for our defense.

Here’s a chart from CBO data. By 2019 the deficit is projected to be $738 billion and rapidly approaching $1 trillion.

Almost every president wants to run for a second term. To forge any hope of being successful with that second run, a president needs to able to say that he or she made a difference on the budget. There are only three ways to reduce the deficit: cut spending, raise taxes, or authorize the Federal Reserve to monetize the debt (or some combination of the three).

At the numbers we are now talking about, getting rid of fraud and wasted government expenditures is a rounding error. But for the sake of the argument, let’s say you could find $100 billion here or there. You are still a long, long way from a balanced budget.

But implicit (and this is critical!) in the CBO projections is the assumption that we will not have a recession in the next 10 years. Plus, the CBO assumes growth above what we’ve seen in the last year or so.

So let’s contemplate what a budget might look like if we have a recession.

The next recession will blow out the budget

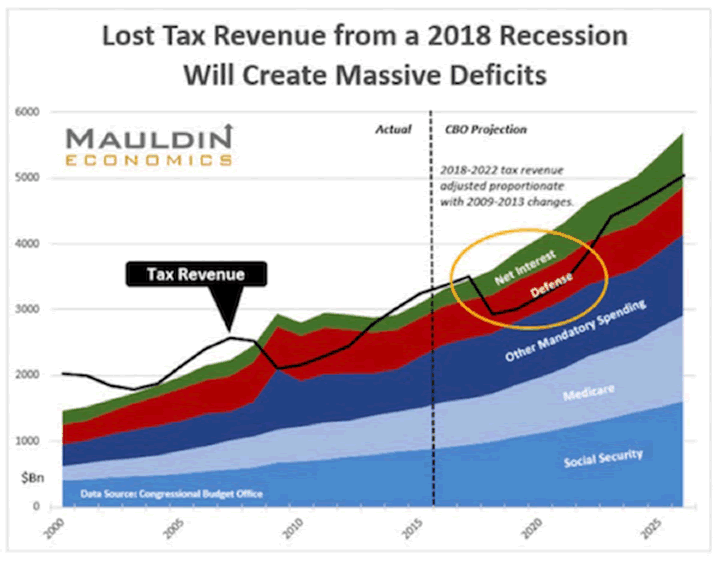

I asked my associate Patrick Watson to look at past recessions and determine what level of revenue losses occurred because of them and then to assume the same average percentage revenue loss for the next recession.

We decided that we would hypothesize our next recession to occur in 2018. If it happens in 2017 or 2019 instead, the relative numbers are the same, and so is the outcome: It would blow out the budget.

Here’s a chart of what a recession in 2018 would do. Entitlement spending, defense, and interest would greatly exceed revenue.

The deficit would balloon to a minimum of $1.3 trillion. And if the recovery occurs along the lines of our last (ongoing) recovery, then unless we reduce spending or raise revenues, we will not see deficits below $1 trillion over the ensuing 10 years.

The deficit will climb to $1.5 trillion, just as the president dives into the thick of a second campaign in 2020. Not exactly a great campaign platform. And that is the known budget deficit. Off-budget additions to the national debt could be as much as one-half trillion dollars.

Bluntly, in such an environment, there’s very little room for infrastructure or stimulus spending. And we desperately need to repair and replace a vast part of our national infrastructure. We have legions of former manufacturing workers and young people whom we need to put to work. And we need to remove as many obstacles to economic growth as possible. We can do all three with an aggressive, Federal Reserve-funded infrastructure program.

Get a Bird’s-Eye View of the Economy with John Mauldin’s Thoughts from the Frontline

This wildly popular newsletter by celebrated economic commentator, John Mauldin, is a must-read for informed investors who want to go beyond the mainstream media hype and find out about the trends and traps to watch out for. Join hundreds of thousands of fans worldwide, as John uncovers macroeconomic truths in Thoughts from the Frontline. Get it free in your inbox every Monday.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.