Trump Rally or Geopolitical Meltdown: Currency Management for Dollar Risk

Currencies / US Dollar May 15, 2017 - 09:15 AM GMTBy: Submissions

The dollar index, which measures the strength of the U.S. currency against a basket of other major currencies, hit a 14-year high on January 3rd of this year. The USD’s reinvigorated bull run after Donald Trump was elected as Barrack Obama’s successor as President of the U.S.A, on expectations for major infrastructure spending and tax cuts during his mandate, has featured prominently in the news. However, the U.S. dollar has more quietly been on an extended rally for a few years now and despite its worst January in 30 years since that early post-New Year peak, many analysts expect that to continue over 2017.

The dollar index, which measures the strength of the U.S. currency against a basket of other major currencies, hit a 14-year high on January 3rd of this year. The USD’s reinvigorated bull run after Donald Trump was elected as Barrack Obama’s successor as President of the U.S.A, on expectations for major infrastructure spending and tax cuts during his mandate, has featured prominently in the news. However, the U.S. dollar has more quietly been on an extended rally for a few years now and despite its worst January in 30 years since that early post-New Year peak, many analysts expect that to continue over 2017.

The Stronger Dollar Scenario

Millennium Global CEO, Mark Astley, recently told CNBC that he expects the dollar to strengthen against the pound to around £1:$1.20 by some point this year as well as achieving at least parity with the euro. In addition to infrastructure spending, loosening of regulations imposed on the finance sector after the global crisis and tax cuts, the Federal Reserve is also expected to raise interest rates by 0.25% two or three times over the course of 2017. This would further strengthen the dollar by making the U.S. a more attractive destination for foreign capital.

The Weaker Dollar Scenario

There is, however, an alternative scenario. Trump has already demonstrated that he has a protectionist inclination when it comes to international trade deals. One of his first actions after taking office was to scrap the Trans-Pacific Partnership, a trade deal the Obama administration had been negotiating for a number of years between the U.S.A and 11 Pacific Rim nations, including Japan and Australia. The deal had finally been agreed upon but not yet ratification by Congress. He also labelled the North American Free Trade Agreement, a trilateral accord between the U.S.A, Canada and Mexico as the ‘worst deal in history’ and vowed to renegotiate or withdraw from it.

Subsequent broadsides which labeled China, and more shockingly Germany, as currency manipulators taking unfair advantage of artificially weak currencies to make their exports more competitive led to a drop in the dollar in January. Many analysts fear that if Trump takes protectionist policies too far it would have a negative impact on economic growth in the U.S.A, hurting the dollar.

The other concern is Trump’s aggressive approach to international relations. He has already provoked divisions with traditional allies and trade partners in Europe and called into question NATO’s continuing relevance and U.S. military spending on European defence. An attempted travel ban for nationals of several Muslim-majority countries, which has subsequently been overruled in court, also caused international outrage. That was followed by a no-compromise stance on news that Iran had tested ballistic missiles, a contravention of the 2015 deal which led to international sanctions against the country being dropped. He immediately raised new sanctions.

Managing Currency Risk

Most market participants and analysts believe the more likely scenario over the next couple of years is a stronger dollar. However, they are also concerned by initial indications that Trump’s presidency might lead to an unwinding of globalization and that he has the potential make decisions and enact policies that would threaten geopolitical stability. An uncertain outlook could also potentially provoke the Fed into reconsidering the pace of the interest rate hikes it is currently planning.

This has led Millennium Global’s Astley to balance his prediction for a stronger dollar with a word of caution:

“Given the uncertainty in the outlook for U.S. interest rates and the path of the U.S. economy after the presidential election, the outlook for the U.S. dollar is far less clear than in the prior three years”.

So, in an environment where there is heightened potential for opposing scenarios on dollar strength over the medium term, how should money managers and other investors manage their foreign currency exposure? Well, there are two main schools of thought on the question:

- Do nothing, currency fluctuations are short term

This approach is comprised of two central tenants. The first is the belief that over the longer term currencies revert to their mean. The second is that for an investor to favour an asset they must also have a positive position on the currency that asset is denominated in as the factors which would lead to that asset appreciating would also strengthen the underlying currency. Ie. investing in a U.S. domiciled asset, or one denominated in dollars, implies faith in the U.S. economy and, subsequently, the dollar.

Taking this school of thought, if assets exposed to the dollar are being held with a longer term outlook and there is no likely requirement for them to be sold on the requirement for short term liquidity, the risk of a dollar weakening on Trump policy can be ignored. It will rebound in time.

There counter argument to this would be that the tenants are simply false. While currency markets can demonstrate cyclical behavior there are numerous examples of permanent shifts in the dynamics between two currencies. Since the U.S.A retired the gold standard in 1971 the dollar has depreciated by over 70% against the Japanese yen. Less permanent multiyear fluctuations from a currency’s long standing mean also have a significant impact on portfolio risk and return even if the mean is eventually reverted to.

The other fallacy is that investing in an asset denominated in dollars necessarily implies faith in the dollar’s strength. Manufacturers that derive a greater percentage of their revenues from markets which don’t use the dollar, or a currency pegged to the dollar, than they do at home would benefit from a weaker dollar, all else being equal. Most portfolios will include an allocation to assets that could foreseeably benefit from the domestic currency weakening. Just look at the gains the UK’s FTSE 100 has seen on the pound weakening since the Brexit vote.

- Hedge Back to the Base Currency

In the second approach money managers take the stance that a return from currency risk attached to investments is uncompensated risk as it is not calculated into the expected return of a portfolio. This category of money manager believes currency markets cannot be accurately predicted so any currency exposure should be completely hedged against and only the relative performance of the asset relied up.

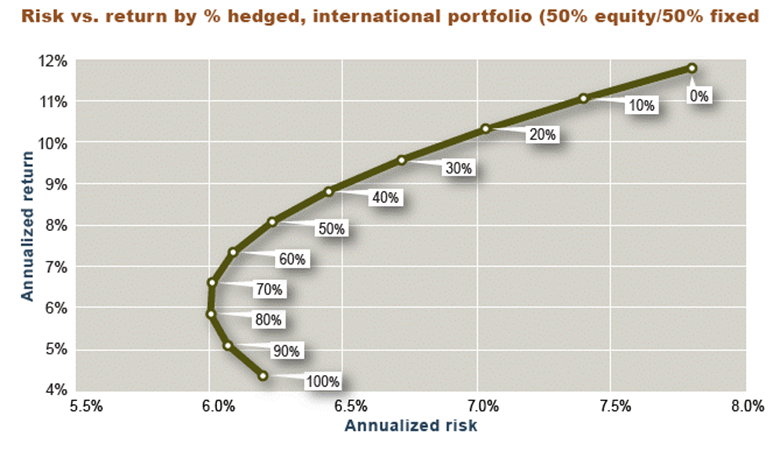

The first objection to this school of thought is that because currency markets are influenced by different drivers than equity and fixed income assets there is often low to negative correlation between a currency and investments denominated in that currency. A perfect example would again be the strong gains the UK’s FTSE 100 has seen since the pound lost value following the Brexit vote. As such, some currency exposure can actually improve the risk profile of a portfolio. The graphic below shows how a portfolio 100% hedged against currency risk carries a higher risk weighting than one that is hedged only 80%:

The other consideration is the cost of fully hedging a portfolio. If the hedge were required to cover a significant period of dollar weakness, the cost would significantly cut into returns.

In answer to the position currency markets are not accurately predictable, there is clear evidence that currency professionals do often consistently predict tendencies in currency movements with enough accuracy to realise a profit.

Currency Management

With neither of these absolute schools of thought the answer to management of dollar exposure in international portfolios, what is? Clearly an active approach is required. Portfolio managers who accept active allocation to hedging currency risk in the same way as they apply active allocation to the other components of their portfolios have two choices.

The first, if the objective is to reduce currency risk, is a dynamic hedging approach. This involves a currency professional increasing and decreasing a portfolio’s hedge in line with anticipated risk levels for the dollar weakening.

The second is to use an active currency overly which is intended to provide a return from currency risk. This approach, if successful, improves the return per unit risk of the portfolio.

Almost all international money managers now recognise the requirement of professional currency management of their portfolios. With the heightened risk of the present geopolitical situation around the dollar’s potential for significant strengthening or weakening, that need is all the greater.

Disclaimer: This is an paid advertorial. This is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors before engaging in any investing and trading activities.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.