The Fed Is at the Height of Monetary Policy Lunacy

Interest-Rates / US Federal Reserve Bank Nov 28, 2017 - 05:10 PM GMTBy: John_Mauldin

How often do central bankers, regulators, corporate leaders, lawyers, politicians, and ordinary investors make the same mistakes over and over again? All the time.

How often do central bankers, regulators, corporate leaders, lawyers, politicians, and ordinary investors make the same mistakes over and over again? All the time.

If we stopped erasing our memories and for once learned from our mistakes, we might make better progress. But no, we must always step on the same rake.

And so the absurdities are perpetuated.

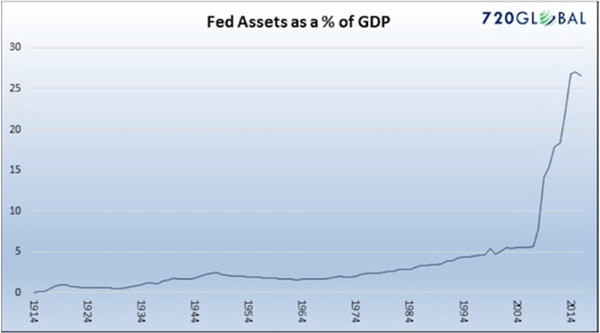

The Growth of Fed Assets since 2008

To kick off our tour of absurdities, Michael Lebowitz of 720 Global sends this chart of Federal Reserve assets as a percentage of GDP. You might notice a slight trend change along about 2008:

Not to put too fine a point on it, but this is bonkers.

I understand that we were caught up in an unprecedented crisis back then, and I actually think QE1 was a reasonable and rational response. But QEs 2 and 3 were simply market manipulation.

The Keynesian Fed economists are dismissive of Reagan’s trickle-down theory. Yet, they applied trickle-down monetary policy in the hope that boosting asset prices would trickle wealth down to the bottom 50% of the US population (aka Main Street).

It didn’t.

Monetary Policy at Whim

The Fed has left that bloated balance sheet alone for almost 10 years. And now for some reason, they feel the urge to reduce it—as they also raise rates. This is not model-based monetary policy. It is simply an emotional monetary policy experiment.

I can understand raising rates—I wish they had done that four years ago. I can even understand reducing the balance sheet. But at the same time? When you don’t know what you don’t know?

I mean really, there is no way to know how the market is going to react to either of these events, let alone to both at the same time. This seems to me the height of monetary policy lunacy.

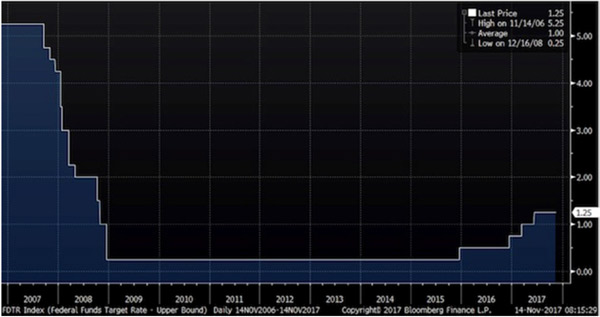

The Fed's stimulus efforts manifested themselves, among other places, in years of near-zero interest rates, helpfully illustrated here by Peter Boockvar:

We all lived through this remarkable set of experiments, but it’s still amazing to think that in 2007–2008 the Fed chopped short-term rates by five full percentage points in just five quarters.

Today we agonize over whether they’ll hike rates by half as much, spread over five years or more. Note also that this gargantuan rate cut still couldn’t avert a near meltdown of the banking system.

You can argue that it would have been even worse to do nothing, but it’s hard to argue they didn’t do all they could have.

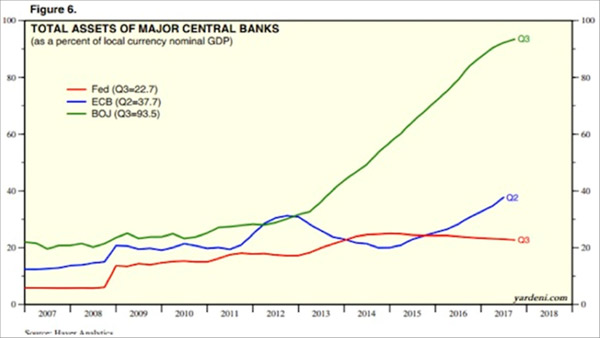

The European Central Bank and the Bank of Japan have both grown their balance sheets more than the US has. The Bank of Japan’s balance sheet is almost five times larger in proportion to GDP.

And it is still growing.

The Land of the Rising Sun has become the land of the rising central bank balance sheet (see the graph below).

The Unthinkable Status Quo

The many shocking, previously unimaginable acts by central banks and governments left us so numb that I think we started to simply accept them without much thought.

That was our mistake.

We must confront the unthinkable, not just shrug our shoulders at it. Because when we have our next crisis, I will bet you dollars to donuts that central banks and governments will react in ways that are even more unthinkable.

Join hundreds of thousands of other readers of Thoughts from the Frontline

Sharp macroeconomic analysis, big market calls, and shrewd predictions are all in a week’s work for visionary thinker and acclaimed financial expert John Mauldin. Since 2001, investors have turned to his Thoughts from the Frontline to be informed about what’s really going on in the economy. Join hundreds of thousands of readers, and get it free in your inbox every week.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.