Gold Minsky Moment Coming

Commodities / Gold & Silver 2020 Feb 26, 2020 - 06:54 AM GMTBy: Richard_Mills

“Minsky Moment” refers to the idea that periods of bullish speculation will eventually lead to a crisis, wherein a sudden decline in optimism causes a spectacular market crash.

Named after economist Hyman Minsky, the theory centers around the inherent instability of stock markets, especially bull markets such as the current one that has been in place for over a decade.

As Investopedia defines it, “A Minsky Moment crisis follows a prolonged period of bullish speculation, which is also associated with high amounts of debt taken on by both retail and institutional investors.”

The Levy Economics Institute of Bard College describes his seminal theory as follows:

“Minsky held that, over a prolonged period of prosperity, investors take on more and more risk, until lending exceeds what borrowers can pay off from their incoming revenues. When overindebted investors are forced to sell even their less-speculative positions to make good on their loans, markets spiral lower and create a severe demand for cash — an event that has come to be known as a ‘Minsky moment.”

There are five stages in Minsky’s model of the credit cycle:

- Displacement – investors get excited

- Boom - bullish speculation, the mania

- Euphoria – extended credit to evermore dubious buyers

- Profit taking – insider/ trader aka ‘smart money’ cashes out

- Bust/ Panic

Two examples of Minsky Moments are the Asian Debt Crisis of 1997, blamed on speculators who put so much pressure on dollar-pegged Asian currencies that they eventually collapsed; and the 2008 financial crisis, which started with the failure of the government to regulate the financial industry, including the US Federal Reserve’s inability to curb toxic mortgage lending, triggering a wave of mortgage defaults and margin calls - as billions in assets were sold to cover debts.

Is the current US stock market, and global economy, approaching a Minsky Moment that pops it? If so, safe-haven assets like gold and silver will surely go ballistic, hence the title of today’s article, ‘A Minsky Moment is coming for gold.’

Let’s take a look at where we are in Minsky’s model of the credit cycle.

US economy - fake and real

Yet you wouldn’t know there’s anything wrong, judging from the US economy. Unemployment is at its lowest in 50 years, wages last year grew by 3.1%, on average, and stock markets keep rolling along.

Although US stocks dropped Tuesday and Apple’s shares took a 2% hit owing to coronavirus-related production problems, the Dow, S&P 500 and Nasdaq are all up significantly, year to date.

Turns out much of this is “fake news”. Marketwatch reported US companies cut back on investment last year, due to reduced exports and disruptions to the global economy from the US-China trade war. For example, spending on new equipment, offices, software etc. rose just 1.3% in 2019 - well short of the 6.4% and 4.4% of 2017 and 2018. While business investment excluding housing is predicted by America’s biggest banks to double this year to 2.4%, that will be offset by an expected 0.5% slowdown in consumer spending.

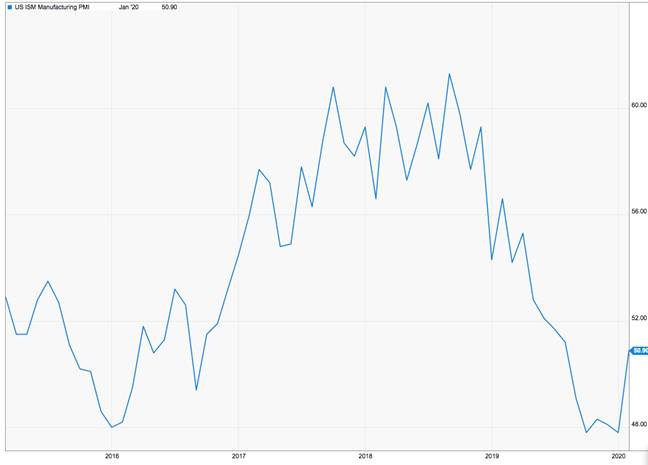

High US stock market performance is masking another economic indicator, that has fallen to its lowest level since 2016 - the purchasing managers index.

The IHS Markit PMI in January fell to a three-month low - from 52.4 in December to 51.7 - barely holding above 50; any reading below 50 indicates poor economic conditions. Firms noted a slower improvement in operating conditions and slack domestic and foreign demand from clients.

And while there are grounds for optimism regarding a trade war resolution, the coronavirus has thrown a spanner into the Phase 1 trade agreement signed on Jan. 15. China’s promise to purchase an additional $200 billion worth of US goods including agricultural products is now in considerable doubt. Beijing is reportedly being urged to invoke “force majeure” - a clause allowing the two parties to consult one another if a natural disaster or force beyond its control delays either party from meeting its obligations under the agreement.

The possibility of moving forward on a Phase 2 agreement also seems unlikely, in light of all the supply chain interruptions caused by the pandemic.

To these trade resolution obstacles, we can add the fact that the Trump administration has just granted its Commerce Department sweeping powers to slap tariffs on countries it decides are manipulating their currencies to the detriment of the United States and its exporting companies.

Buybacks

As we have written, share buybacks are a relatively new phenomenon. For most of the 20th century they were illegal because they were considered to be a form of stock market manipulation. But that all changed in 1982 when the SEC legalized them. Since then buybacks have been a popular tool for management to stuff cash back into the company, indirectly, by reducing the share float.

Purchasing company stock generally inflates the share price and boosts earnings per share – a key metric on which CEO bonuses are calculated. After the SEC changed the rules to allow buybacks, hundreds of companies starting using them. In 1997 buybacks surpassed dividends as the main way companies redistribute funds to investors.

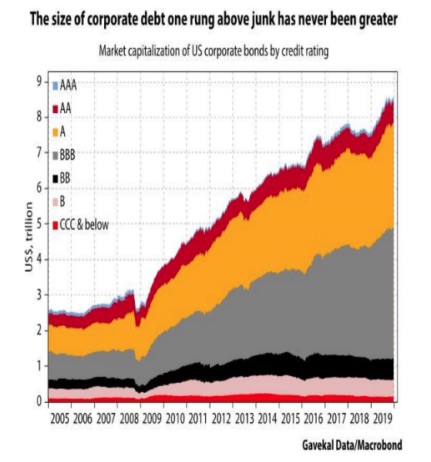

Buybacks are the main reason for the extraordinary rise in the S&P 500 since 2009. According to a blog by Evergreen Gavekal, a registered investment advisor (RIA), while there is nothing inherently wrong with share repurchases (reducing a company’s outstanding shares makes each dollar of earnings more valuable on a per share basis, which is good for investors), the problem is that companies are borrowing at an alarming rate in order to repurchase their own shares.

Evergreen Gavekal explains:

As the high-profile economist David Rosenberg has repeatedly pointed out, there is a $4 trillion trifecta occurring presently. During the twenty-teens, the Fed has created $4 trillion of – to be blunt – “Bogus Bucks”, or BBs, and those BBs have been used to fund $4 trillion of other BBs, as in buybacks, and yet another $4 trillion has been taken out in additional corporate debt (a third BB, Bubble Bonds?). Kind of a strange coincidence, isn’t it?

To elevate debt to dangerous levels to enable share repurchases—which usually lowers profits because of the increased interest costs—is the antithesis of judicious corporate stewardship. Again, this likely won’t become an issue until the next recession—a full-blown one, not just of the earnings and industrial variety. But when that occurs, the trap door will fly open and the plethora of corporate bodies left twisting in the wind will be a gruesome sight.

When companies are repurchasing shares at one of the highest levels ever relative to the size of the US economy, and also compared to cash flow, they are almost certainly destroying long-term value for their shareholders.

Not only is shareholder value being destroyed through copious share buybacks, there is also record insider selling going on. According to the SEC, insiders typically sell five times as much stock in the eight days after a buyback announcement as ordinary days.

“The big picture view of this situation is that we have companies repurchasing their shares at a fever pitch while insiders are dumping said shares at an equally feverish rate,” states the blog, adding that the “death-knell of buybacks” could be the high corporate debt levels compared to the rest of the economy (US companies are currently sitting on nearly $10 trillion in debt, close to half (47%) the value of the rest of the economy). Alternatively, they could be canceled by legislation should the Democrats gain power in November’s elections.

If something were to happen to stop, or restrict the practice, the Minsky Moment would almost certainly come about via a stock market crash the likes of which we may not care to envision.

Inflection

In our recent article we said we believe the global economy has reached an inflection point. Global growth has slowed, compounded by trade wars, the slowdown in China, and the latest threat – the coronavirus. What will it take to push it over the edge? We’ll get to that but first, consider the defensive stance being taken by gold-backed ETFs and central banks.

According to the World Gold Council “Global gold-backed ETFs and similar products added 61 tonnes(t), or net inflows of US$3.1bn, in January across nearly all regions, boosting holdings to new, all-time highs of 2,947t.”

Central banks, worried about economies cooling and low inflation, were buying gold by the truckload and pursuing monetary stimulus, in the form of interest rate cuts and/or massive bond-buying programs like we went through with quantitative easing in the US, Europe and Japan.

That worked pretty well after the financial crisis, when the world economy was more or less back on track, with no tit-for-tat tariffs impeding international trade, and the US dollar still carrying enough heft and respect to enjoy exorbitant privilege.

This time is different. We have an unpredictable president in the White House that has already done much damage to the world economy, hurt the relationship between the US and China, and now appears heading towards a global currency/ trade war wherein everybody dukes it out over who can devalue and out-export the other. The outcome is a gradual race to worthless and America’s trading partners punting the dollar and replacing it with a basket of currencies, likely (remember all that Central Bank gold buying) backed by gold.

So, what might be the hair trigger that causes the US stock market bubble to pop and gold to soar? It’s impossible to know for sure, but we can take a few educated guesses based on what we know is happening in the global economy, as we write.

Pandemic effects

All eyes are on the coronavirus and its economic repercussions, particularly on the Chinese economy and the economies of China’s closest trading partners.

Quarantines, done to contain the outbreak, have had an impact on global supply chains including mined commodities. Earlier this month, China’s copper buyers asked Chilean miners to delay shipments due to port shutdowns. Ocean freight carriers are refusing to dock in China, same as airlines have canceled flights. Some mining companies have had trouble delivering supplies due to transportation blockages and delays.

China’s home prices have fallen and large swathes of Chinese industry have not re-opened after Chinese New Year because migrant workers, afraid to return to the cities, are staying in their home villages. The loss of these workers/ shoppers has dented China’s increasingly consumer-oriented economy.

Although coronavirus is mostly confined to Hubei province and Wuhan, the city of 11 million people known to be the epicenter, medical experts are not ruling out the virus fanning out beyond the 24 countries currently affected. Bloomberg ran a story saying it could infect a shocking two-thirds of the globe.

Traders are reportedly piling into hedges if the contagion becomes a disaster for the global economy which is already limping along. In its January update, the IMF lowered its 2020 global growth forecast by one-tenth of a percentage point to 3.3% - following last year’s 2.9%, the lowest in a decade.

In Japan, GDP has fallen a precipitous 6.3%, nearly twice as much as the predicted 3.7% - catalyzed by poor weather and a hike in the sales tax. Notably, the coronavirus was not a factor in the dismal figure, meaning the outbreak could take an even worse toll on the world’s third-largest economy.

Last year Germany slipped into a manufacturing recession and the largest economy of the Eurozone area does not appear to be improving. The Guardian reported the German economy flat-lined to 0% growth in the fourth quarter - side-swiped by lower exports on account of trade tensions, and a slowdown in consumer and government spending.

If the coronavirus continues to be a problem, many are expecting the Fed will step into lower interest rates.

“The impact of the virus on the global economy is going to be significantly more than what people are expecting, and when the global economy goes south, the Fed steps in,” BNN Bloomberg quoted Tony Farren, managing director at broker-dealer Mischler Financial in Stamford, Connecticut.

One signal of a potential reduction, beyond the 1 to 2 quarter-point cuts already priced into the market, is the spread between 2- and 10-year Treasury yields, currently at the flattest level since November. A yield curve inversion, when short-term yields push higher than long-term yields, is a predictable recession indicator.

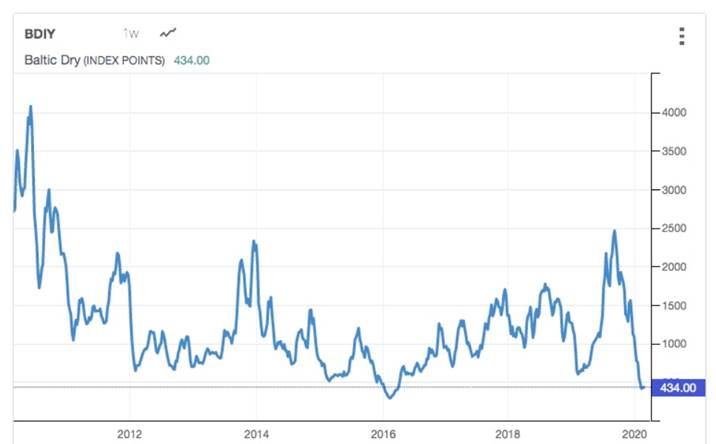

Shipping collapse

One of the most alarming sign of the world economy’s malaise is the Baltic Dry Index chart. From 2500 in September the BDI has plunged over 80% to 434, meaning the cost of shipping is one-sixth what it was 5 months ago. According to Hellenic Shipping News, rates for Capesize bulk vessels are less than a third of breakeven and the BDI is fast approaching the 290 points of February 2016 - the worst of all time.

Currency Rule

The Trump administration is going down a very dangerous road with its new Currency Rule that imbues the US Commerce Department with incredibly strong powers to invoke across-the-board trade protectionism from countries all the way down to individual companies. The way we see it, buying gold or silver bullion is one of the best ways to take a defensive position during what could be the beginning of an all-encompassing trade war and a truly global, and a round of highly competitive currency devaluations, wherein the winner is the biggest loser.

Some industries, and us at AOTH, believe this aggressively protectionist stance will lead to currency wars and turn the $6 trillion per day global currency market into a new battleground for Trump’s trade wars.

Goods benefiting from weak currencies, representing each and every one of America’s trading partners, could be recipients of duties or countervailing duties, equal to the difference between the weaker currency and the US dollar - in other words, eliminating that country’s currency advantage.

While China is the obvious target of US tariffs, and rule changes strengthening the Commerce Department’s hand in dealing with currency complaints, there are many other countries, and individual businesses Commerce has in its sights.

Last year the Treasury Department came out with a report that recommended 21 trading partners should face scrutiny over their currencies - they include China, Germany, Japan, South Korea, Ireland, Italy, Malaysia, Vietnam and Singapore.

These trading nations, and even their individual businesses that import goods into the US, are now vulnerable to being tariffed on targeted imports - an amount that will make imports sell for more than their US counterpart.

Geopolitical risk

Other potential catalysts, aka Minsky moment, for gold are geopolitical. In a Project Syndicate article economist Nouriel Roubini points to “white swan” events (they are knowable versus unknowable “out of the blue” black swans) that could turn the current boom and bubble into a crash and burst. White swans include the US rivalries with China, Russia, Iran and North Korea:

These countries all have an interest in challenging the US-led global order, and 2020 could be a critical year for them, owing to the US presidential election and the potential change in US global policies that could follow.

Under President Donald Trump, the US is trying to contain or even trigger regime change in these four countries through economic sanctions and other means. Similarly, the four revisionists want to undercut American hard and soft power abroad by destabilizing the US from within through asymmetric warfare. If the US election descends into partisan rancor, chaos, disputed vote tallies, and accusations of “rigged” elections, so much the better for America’s rivals. A breakdown of the US political system would weaken American power abroad.

Arguably, the US political system is already broken, which substantially ups the chance of some kind of clash with one of these four powers. A dysfunctional polarity of views that has become the norm in US politics. We have written before on how this extreme polarization is killing America.

The real disaster is the fact that partisanship is preventing legislators from working together to solve important issues - like addressing the ways that climate change is set to wreck US coastal cities, or reforming mining legislation to make America less dependent on foreign suppliers of critical minerals.

We’ve noticed the partisanship, the bickering, the impasses, the sheer hatred of the other side, is worse under Trump, who certainly fanned the flames of discord to get elected, and continues to blow on them, knowing that divide and conquer is his best path to re-election in 2020.

Things aren’t much better with the Democratic Party, though. The division within the Dems has been evident since the first debates last summer, as a slew of candidates duked it out over how far the party should migrate to the left, to win back the White House. There are still eight candidates vying for their party’s nomination as they head into the Texas primary.

Roubini thinks conflict between the US and Russia, China, Iran or North Korea could occur through some form of cyberwarfare. Russian hackers are known to have interfered in the 2016 election. The same thing could happen again in 2020 - possibly from China as retribution for the US being a trade irritant. The four may also gang up Western financial systems such as the SWIFT platform - used by banks and financial institutions to clear international monetary transactions.

The current arms buildup between the US, China and Russia, precipitated by the US pulling out of the 1987 INF Treaty due to Russia breaking its terms, could easily trigger a war especially if China is pushed into a corner due to economic weakness and is looking for a scapegoat. Taiwan, Hong Kong, Vietnam and US naval positions in the East and South China Seas are all potential hot spots that could lead to military confrontation, Roubini writes.

That, combined with persistent trade barriers that are keeping the Chinese economy weak, could result in China dumping US Treasuries. If there was ever a Minsky Moment, this would be it.

But instead of selling Treasuries and converting dollars into renminbi, causing the latter to rise, choking off Chinese exports, Roubini points out the Chinese could instead convert their dollars into gold. This would both add to its central bank gold reserves - something China continues to do - while hurting the US economy:

In a sell-off scenario, the capital gains on gold would compensate for any loss incurred from dumping US Treasuries, whose yields would spike as their market price and value fell. So far, China and Russia’s shift into gold has occurred slowly, leaving Treasury yields unaffected. But if this diversification strategy accelerates, as is likely, it could trigger a shock in the US Treasuries market, possibly leading to a sharp economic slowdown in the US.

Debt

Meanwhile in November, total US debt surpassed $23 trillion for the first time, with just under $17 trillion held by the public and $6 trillion in government loans.

“Reaching $23 trillion in debt on Halloween is a scary milestone for our economy and the next generation, but Washington shows no fear," The Hill quoted Michael Peterson, CEO of the fiscally conservative Peter G. Peterson Foundation.

“Piling on debt like this is especially unwise and unnecessary in a strong economy,” he added.

The country is accumulating about the same amount of debt as its annual economic output. Each year another trillion dollars gets added to the national debt.

Rising interest rates compound the problem. In 2008 interest on the national debt was $253 billion, and consumed 8.5% of the federal budget. In 2019 the government had to put aside $376 billion in debt interest, a third of the real defense budget, and more than spending on education, agriculture, transportation and housing combined.

By 2026 the interest is projected to be $762 billion and take up 12.9% of the budget.

According to its latest projections, the Congressional Budget Office says debt-to-GDP will reach 150% by 2047, well past the point where financial crises typically occur. The budget deficit is also likely to rise, nearly tripling from 2.9% of GDP to 9.8% in 2047. The growing debt burden is not just a US phenomenon; it’s global.

In the first quarter of 2019, world debt hit $246.5 trillion, reversing a trend that started in the beginning of 2018, of reducing debt burdens, when global debt reached its highest on record, $248 trillion.

This can’t go on forever. It’s not a stretch to envision a scenario whereby the world’s reserve currency, the US dollar, collapses under the weight of unmanageable debt, triggered say, by a mass offloading of US Treasuries by foreign countries, that currently own about $6 trillion of US debt. This would cause the dollar to crash, and interest rates would go through the roof, choking consumer and business borrowing. Import prices would skyrocket too, the result of a low dollar, hitting consumers in the pocket-book for everything not made in the USA. Business confidence would plummet, mass layoffs would occur, growth would stop, and the US would enter a recession.

All the countries that sold their Treasuries would then face a major slump in demand for their products from American consumers, their largest market. Eventually companies in these countries would begin to suffer, plus all other nations that trade with the US, like Canada and Mexico. Before long the recession in the US would spread like a cancer, to the rest of the world.

This of course is a likely scenario to gold enthusiasts who invest and believe in gold for its utility as a store of value when everything else - ie. fiat currencies - fails. Indeed holders of dollars would find their once-powerful greenback reduced to monopoly money. People with gold would be the only ones left with any purchasing power to pay bills and buy day-to-day goods and services.

Conclusion

Consider what happened to gold when Iran countered the assassination of its top military commander with missile strikes against two Iraqi bases housing US troops.Gold futures jumped to a six-year high of $1,613.30 an ounce, as fear and uncertainty over what comes next had investors piling into the precious metal.

Think of that as a dress rehearsal for what could really cause a spike in gold - including but not limited to: the collapse of the US dollar underneath a mounting pile of debt; the end of stock buybacks, responsible for much of the air inside the decade-long US stock market bubble; an escalation of the trade war between the US and China, made worse by new tariff-levying powers granted to the US Commerce Department; or even a shooting war that erupts out of a geopolitical conflict such as Hong Kong, Taiwan or Chinese territorial ambitions in the South China Sea.

This article has presented some of the “Minsky Moment” scenarios that could set the gold price on a tear the likes of which we’ve never seen.

I’d like to end this article here, after presenting you not with the disease we suffer, but with its symptoms/ consequences, and take the following up, in another article.

“all the effort and planning imaginable cannot make paper money work. There is no way paper can be "improved" as money. Whenever governments are granted power to purchase their own debt, they never fail to do so, eventually destroying the value of the currency.”Ron Paul, The Case for Gold

As investors, the best way to protect ourselves against a global (or regional, depending on where you live) calamity that even a large cache of US dollars could fail to provide, is to own gold.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2020 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.