The 50th Anniversary of Nixon’s Colossal Gold Standard Error

Commodities / Gold and Silver 2021 Mar 18, 2021 - 03:41 PM GMTBy: Richard_Mills

It seems fitting that the year we are expecting to see an unprecedented rise in US government spending and money-printing to spur an economic recovery, marks the 50th anniversary of the end of the gold standard.

Done at the time to fight an economic crisis, we are still feeling the effects of this disastrous decision, five decades on.

In this article, we explain why President Nixon did what he did, and why every promise that unshackling the US government from the requirement of maintaining the dollar’s value in terms of gold would mean for the United States, has been broken.

Killing the gold standard

It all started with Nixon, and the economic problems he inherited from the preceding Kennedy-Johnson administration.

Nixon was no social democrat, very much the opposite; a conservative Republican who criticized government intervention in the economy, he believed in small business and small government.

Yet Nixon was haunted by his loss to John Kennedy in the 1960 election, which he blamed on a recession that year.

And he saw the recession as the fault of “financial types” who prioritized lowering inflation over reducing unemployment.

Then-Federal Reserve Chairman Arthur Burns had warned Nixon in 1960 that the Fed’s tight monetary policy would exacerbate the economic downturn and threaten Nixon’s chances against his young, telegenic competitor, Democrat John Kennedy. This is exactly what happened.

The mercurial president was not going to let that happen again.

So, when Nixon looked ahead to re-election in 1972, he was hyper-conscious of the state of the economy, which by 1970, was not looking so good.

To some extent Nixon could blame the problems on the previous Johnson administration. Ambitious agendas like the War on Poverty and the Great Society, along with escalating (but not winning) the Vietnam War, added $42 billion to the national debt, more than double the amount added by JFK.

In 1968, President Johnson’s spending boosted economic growth to 4.9% but inflation hit a disturbing 4.7%. As Americans prospered, they imported more goods, creating a huge balance of payments deficit.

The excess of dollars in the global economy threatened the gold standard, whereby the Federal Reserve redeemed US$35 for an ounce of gold. As explained by The Balance,

In 1968, the United States had over $45 billion in federal reserve note liabilities but held only about $10 billion in gold. It was not enough to redeem the liabilities. Foreign holders turned in their dollars for gold, depletingcentral banks’ gold reserves even more.To make the dollar more attractive to hold, the Federal Reserve raised interest rates to 6%.

But the run-on gold continued. It boosted inflation to 6.2% in 1969, Nixon’s first year in office.TheFed defended the gold standard by raisingratesto 9.19%. Unfortunately, it also created a mild recession that started later that year. By the end of 1970, the unemployment rate had risen to 6.1%.

This was not a theoretical construct. The mismatch of dollars to gold meant that governments or their central banks could show up at any time to the US Treasury’s “gold window” and demand gold for dollars. In August 1971, the British Ambassador did just that, requesting that $3 billion be converted into gold.

In 1970 Burns declared that the economy was no longer operating as it used to, due to the growing power of corporations and unions, which together, were driving up wages and prices. The answer, in Burn’s view, was to impose wage-price controls, wherein an appointed wage-price review board would pass judgment on major wage and price increases.

As Nixon looked towards re-election in ’72, he wasn’t going to let the economy bring him down again in a repeat of 1960.

As PBS describes in an excellent essay titled ‘Nixon, Price Controls and the Gold Standard’, The central economic issue became how to manage the inflation-unemployment tradeoff in a way that was not politically self-destructive; in other words, how to bring down inflation without slowing the economy and raising unemployment.

To figure out a way forward, Nixon and 15 advisors repaired to the presidential mountain retreat at Camp David. The answer was the New Economic Policy, wherein wages and prices would be frozen for 90 days as a way of attacking inflation. The idea was that wage-price controls would allow the administration to pursue a more expansive monetary policy, thereby stimulating employment in time for the 1972 election without stoking inflation.

“Now I am a Keynesian,” Nixon declared in January 1971, before introducing a “full employment” budget, which provided for deficit spending to reduce unemployment.

More ominously, the gold window was to be closed, something Arthur Burns disagreed with. “Pravda would write that this was a sign of the collapse of capitalism,” he warned, but was over-ruled.

Closing the Treasury’s window for gold redemptions immediately weakened the dollar, which added to inflation by driving up the prices of imported goods. As the PBS essay reminds us, Going off the gold standard and giving up fixed exchange rates constituted a momentous step in the history of international economics.

How to account for Nixon’s “conversion” to intervening in the economy, something previously anathema to his political philosophy?

The president reportedly was tormented, as he wrote his Aug. 15, 1971 “Nixon Shock” speech, over whether the press would judge him to have acted boldly, or to have changed his mind.

“Having talked until recently about the evils of wage and price controls,” Nixon later wrote, “I knew I had opened myself to the charge that I had either betrayed my own principles or concealed my real intentions.”

“Philosophically, however, I was still against wage-price controls, even though I was convinced that the objective reality of the economic situation forced me to impose them.”

In the end, his doubts were put to rest; the speech was a hit.

“Prosperity without war requires action on three fronts: We must create more and better jobs; we must stop the rise in the cost of living; we must protect the dollar from the attacks of international money speculators,” Nixon pronounced.

The public ate it up, with many feeling that the government was coming to their defense against price gougers, and that international speculators had been dealt a deadly blow.

Closing the gold window was controversial, but the naysayers were shouted down, and Nixon was re-elected in 1972, winning every state except Massachusetts.

Aftermath

As for wage and price controls, they did not work. In the months that followed Nixon’s re-election, inflation picked up again, and in 1973, another wage and price freeze was implemented. As PBS describes, This time, however, it was apparent that the control system was not working. Ranchers stopped shipping their cattle to the market, farmers drowned their chickens, and consumers emptied the shelves of supermarkets.

Wage-price controls created a recession in November 1973 and led to three consecutive quarters of negative GDP growth.

Most of the system was abolished in 1974, four months before Nixon resigned in disgrace, a victim of Watergate.

In May of 1975, unemployment hit 9%.

How will Nixon be judged for ending the gold standard? As it turns out, quite harshly.

In 1973 the president devalued the dollar, making an ounce of gold worth $42 instead of $35. This resulted in a selloff in greenbacks for gold, and by the mid-1970s inflation was in the double digits. Later in ‘73 Nixon decoupled the dollar from gold completely, which made the price of bullion soar to $120 per ounce and ended the 100-year history of the gold standard.

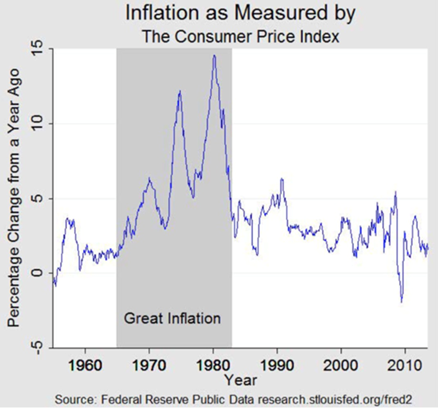

Quitting the gold standard resulted in stagflation. Falling growth + high inflation + high unemployment was only cured by double-digit interest rates which caused the 1981 recession.

Removing the dollar’s peg to gold also opened the door to allowing the US government to print money to solve every economic problem, ensuring the greenback’s value would fall indefinitely. This is exactly what has happened.

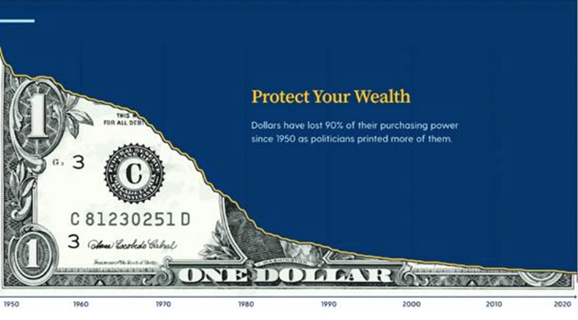

In the US there was an increase in inflation for every decade except the Depression when prices shrunk nearly 20%. The Bureau of Labor Statistics’ Consumer Price Index indicates that between 1860 and 2015, the dollar experienced 2.6% inflation every year, meaning that $1 in 1860 was equivalent to $27.80 in 2015. The dollar has lost 90% of its purchasing power since 1950.

A lot more can be said of the aftermath of Nixon’s gold standard decoupling, which when it comes down to it, was only done to ensure his re-election.

As Forbes wrote in 2011, No other single action by Nixon has had a more profound and deleterious effect on the American people. In the end, breaking the solemn promise that a dollar was worth 1/35th of an ounce of gold doomed his Presidency, and marked the beginning of the worst 40 [now 50] years in American economic history.

First, the promises. Economic wisdom at the time held that unshackling the dollar from gold would let the Fed manipulate the levers of monetary policy to increase the nation’s prosperity. Domestically, that meant no more costly recessions, high employment, and robust economic growth. Internationally, a devalued dollar would improve US competitiveness through cheaper exports, thereby creating jobs.

Each one of these promises has been broken.

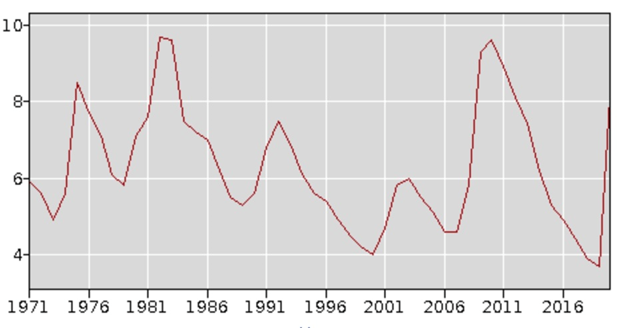

In the 50 years since the gold standard was eliminated, unemployment has stuck above 5% in all but 12 years. The worst jobless rates, as seen in the graph below, were during recessions in 1982-83 (9.7% and 9.6%), 2009-10 (9.3% and 9.6%) and 2020 (8.1%).

Source: US Bureau of Labor Statistics

These figures look particularly bad when compared to the gold standard era. Between 1947 and 1970, unemployment averaged less than 5% and never rose above 7%.

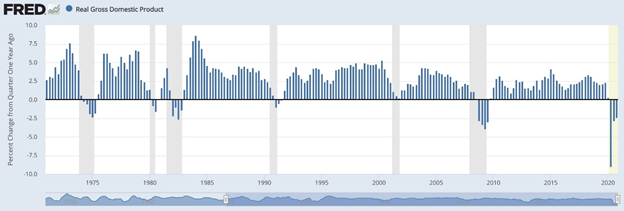

Economic growth has been sluggish too. Whereas GDP grew 4% a year during the post-War gold standard period, between 1971 and 2011, real economic growth (after inflation) averaged 2.9%, compared to 4% during the gold standard era. From 2011 to 2020, real GDP as seen in the FRED chart below (percentage change from Q1 the previous year) only goes above 2.5% in 15 of 45 quarters.

Source: St. Louis Fed

As Forbes points out, 1% may not seem like a big difference, but it’s actually huge. An economy growing at 3% creates just enough jobs, but 4% puts a dent in the unemployment rate. Moreover, at 3% growth, the US economy is about $8 trillion smaller than if it was growing at 4%, implying median income of about 50% higher than it was in 2011.

The tax base would be 50% bigger as well.

As mentioned, the severing of the link between the dollar and gold has meant a buck whose value is in terminal decline. Yet it has not, as promised, made the US more competitive.

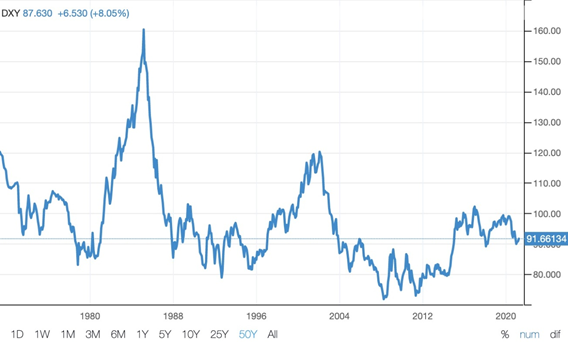

From a 50-year high of 162 in 1985, the US dollar index DXY — which measures the value of the dollar against a basket of six currencies, the euro, Swiss franc, Japanese yen, Canadian dollar, British pound, and Swedish krona – has fallen by 184%.

Source: Trading Economics

In 2011, Forbes notes, the dollar had lost about 80% of its purchasing power, worth under $0.20 compared to the pre-Nixon dollar.

By contrast, a gold standard is extraordinarily good at maintaining the buying power of the dollar. From 1948 to 1967, inflation averaged less than 2% per year. Interest rates were low and stable, with the yield on AAA corporate bonds averaging less than 4%, providing a reasonable cost of funds to borrowers, and a fair return to savers.

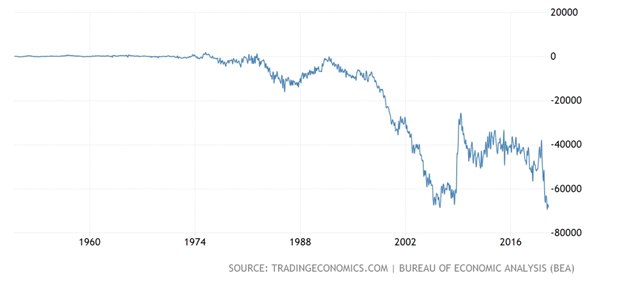

The US had a modest export surplus before Nixon started the dollar on its downward path; in 2020 the trade deficit reached $678.7 billion, according to the US Bureau of Economic Analysis, and that was after the Trump administration started (but never finished) a trade war with China and several of its trading partners, designed at lowering the trade deficit.

Source: Trading Economics

The real shocker though comes when evaluating the price of commodities, viz a viz the devalued dollar. Forbes calculates that in 2011, if the dollar had continued to be worth 1/35th of an ounce of gold, a barrel of oil would sell for less than $2.50. The price of a barrel of WTI crude topped out at $106.11 in March 2011. Today the same barrel of WTI, worth $65.56, would sell for $1.32 in pre-Nixon dollars.

That’s right, the whole notion of an energy crisis and the ever more intrusive government regulations dictating energy usage are based on the grand illusion that the price of oil has gone up more than 30 fold when in fact, it is the dollar whose value has fallen relative to gold, oil, and all other goods and services over the past 40 years.

The final indignity of the beleaguered US dollar concerns the fact that, between 1947 and 1967, there was only one currency crisis, no major bank failures, or corporate bailouts.

Since Nixon killed the gold standard, there have been 13 financial crises, including the 1973 oil shock, the financial crisis of 2008-09 and the coronavirus crisis of 2020-21.

As Forbes concludes,

The evidence is in. The great experiment of a paper dollar managed by able men and women has failed and failed miserably to keep any of its promises.

Our conclusion at AOTH is much the same. Nixon was persuaded, against his better judgment, to try beating inflation in 1971 by imposing wage and price controls. He did this essentially to get re-elected. But Nixon went further in committing what must be seen in retrospect as a colossal blunder in removing the fixed link between the dollar and gold.

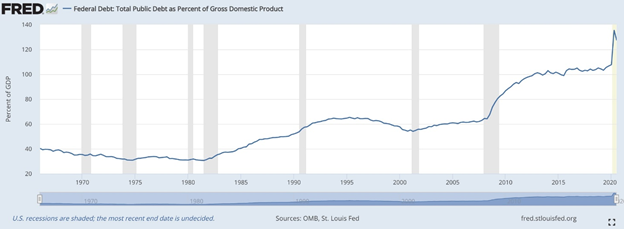

The move killed the dollar, which has been losing value ever since. Why? Because successive governments and central banks have taken it upon themselves to create money (ie. the Fed) and spend money (the Treasury) with no consequences, something that could never happen if the dollar had a gold anchor. Going back to it, monetary/fiscal policy would be much restricted, for sure, but neither could the federal government be allowed to run up the debt to its current $28 trillion, in the fall of 2020 exceeding the debt to GDP ratio by 100% for the first time since the Second World War.

Source: OMB, St. Louis Fed

There would also be no unfettered growth of the money supply, which is inflationary, and no expansion of the Fed’s balance sheet to over $7 trillion.

Nixon’s historic decoupling of gold and the dollar has important ramifications for the current US economy, and investors.

What happens when people realize the federal government has depreciated the greenback by spending $6.5 trillion using borrowed money, plus the Fed’s $7 trillion, meaning the purchasing power of the dollar has been cut in half? The equivalent of half the $28-trillion national debt? And with trillions more debt to come, at AOTH we believe there is only one direction for the dollar, and only one way for gold.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2021 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.