Pick up in UK house price growth seals a May interest rate rise

Housing-Market / UK Housing Apr 26, 2007 - 11:49 PM GMTBy: Nationwide

Pick up in house price growth seals a May interest rate rise

Pick up in house price growth seals a May interest rate rise

• Pace of house price growth picks up in April, but trend still shows a gradual cooling

• Market demand has been supported by movers, but this too is beginning to wane

• Too rapid an increase in rates could destabilise the market

• Current economic conditions suggest that a house price crash is unlikely

Commenting on the figures Fionnuala Earley, Nationwide's Chief Economist, said:  “The Bank of England held off raising rates at the beginning of April, but the acceleration in house prices

during the month makes a rate rise on the MPC’s 10th anniversary look like a certainty. The pace of house

price growth almost doubled during April to 0.9%, up from 0.5% in March. This brings the annual rate of

“The Bank of England held off raising rates at the beginning of April, but the acceleration in house prices

during the month makes a rate rise on the MPC’s 10th anniversary look like a certainty. The pace of house

price growth almost doubled during April to 0.9%, up from 0.5% in March. This brings the annual rate of

inflation back into double digits at 10.2% and the price of a typical house up to £180,314, which is £16,741

higher than at this time last year.

“However, while the monthly rise in prices is stronger than the MPC would have liked to see, it can take some comfort from the fact that the underlying trend is softening and the return to double-digit annual growth largely reflects a weak period this time last year. The three-monthly growth rate, which smoothes the volatility of the monthly series, is still cooling in response to the earlier rises in interest rates. The latest figures show prices increased by 2% between February and April, the lowest three-monthly growth rate since last August.

Caution against sharp rate rises which could destabilise the market

“While a stable economic environment with contained inflation is essential for a well behaved housing market,

we would caution against too sharp an interest rate response to current economic data. In our view, the talk

of rates climbing to 6% and beyond are overblown and if implemented in the current climate could be

damaging to housing market stability. With the market already showing signs of cooling, too sharp a rate hike

could undermine market confidence and dry demand up swiftly. But on top of this, the could also lead to

widespread payment difficulties which, in an illiquid market, could precipitate price falls.

Movers have supported market demand…

“Housing demand has been resilient, but there are signs that this is beginning to wane across the board. During 2006 there were 43,000 more first-time buyers than in the previous year and 56,000 more buy-to-let purchasers. But existing homeowners trading mongst themselves were even more active with an increase of more than 84,000 purchases. However, affordability for those entering the market has deteriorated and led to a fall in the numbers jumping onto the housing ladder more recently. Between December 2006 and February2007, 3,200 fewer first-time buyers managed to get onto the ladder compared with the same period a year earlier. Even demand from movers may now be beginning to moderate with 2,500 fewer movers in February compared with the previous month.

…but are not immune to interest rate rises

“These existing homeowners, many with large amounts of equity as they purchased their property prior to the

recent house price rises, have been able to continue to trade for longer as they could absorb some of the

transactions costs such as stamp duty, deposits and fees in new mortgage borrowing. But they are not

immune to further interest rate rises. As the amount borrowed has increased, so will the impact of rises in

interest rates on their mortgage payments. Levels of mortgage equity withdrawal have also been increasing

adding to overall debt levels and ratcheting up the impact of further rate rises.

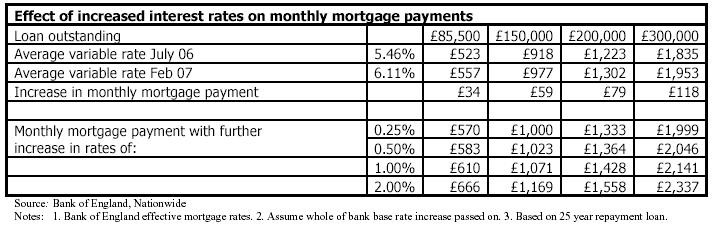

“57% of the total number of people with a mortgage have a variable rate mortgage. Since July, the average rate payable has increased by 0.65% (less than the 0.75% increase in the base rate) from 5.46% to 6.11%. The average amount outstanding on a mortgage at the end of 2006 was £85,500 which means that the combined increases in mortgage rates have added only about £30 per month to the monthly payment. However, the average includes some very old loans and low value loans. More recent borrowers will have faced a much larger increase in monthly payments. A variable rate loan of £150,000 for example would already have seen an increase of around £60 and one of £200,000, £80 per month.

“At this level, the past increases are not insignificant, but should be manageable, especially as larger

borrowers tend to take out fixed rate loans. Indeed, 76% of all house purchase and remortgage loans were

taken out on a fixed rate in February. However if the MPC was to hike rates sharply there is a risk that many

borrowers on popular tracker rate products could find themselves with payment difficulties. A further 1%

increase in rates would mean an extra monthly payment of £153, compared with pre-rate rise payments on a

£150,000 loan – an increase of 16.7%. This could clearly be quite uncomfortable for some, and those coming

off fixed rate loans priced at around 4.99% two years ago would face an even greater payment hike of around£200 per month.

House price crash predictions are premature

“Some commentators are already suggesting that the market is poised for a fall with affordability so stretched, especially for first-time buyers. At a simplistic level, a move in the house price to earnings ratio back to its long term average would imply a fall in house prices of nearly 40%. However, the long term average house price to earnings ratio is not a good benchmark given that we would expect this ratio to trend upwards over time. Reasons for this include the decline in real and nominal interest rates since the 1980s and a change in people’s preferences towards housing as an investment, as a supplement or alternative to equity based pensions. In addition, as we have mentioned several times, the UK suffers from a slow response of housing supply to changes in demand, which supports house prices. Looking at mortgage payments as a proportion of take home pay, which takes lower interest rates into account, suggests that rates could increase by more than 2% before affordability (on this measure) became as stretched as in the late 1980s.

“A more important factor which would suggest that large price falls are unlikely in the current economic

climate is the state of the general economy. Clearly there are risks to interest rates, but in the current

circumstances it is not clear how big these are. Even the tone of Mervyn King’s letter to the Chancellor and

his testimony to parliament seemed fairly sanguine. In both cases the Governor expressed the view that CPI

inflation could fall back sharply over the next four to six months, which would suggest severe rate hikes are

unlikely. Back in the 1980s the collapse in prices came about following a sharp rise in interest rates (from

7.4% in mid 1988 to around 15% two years later) and a 1.4m increase in unemployment at a time when the

economy was slowing. Today the economy is continuing to grow; the labour market has been remarkably

strong and interest rates have increased by only 0.75% in the last two years.”

By Fionnuala Earley

Chief Economist

Tel: 01793 656370

fionnuala.earley@nationwide.co.uk

Katie Harper

Press Officer

Tel: 01793 656215

katie.harper@nationwide.co.uk

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.